Organizational conflict is sometimes unavoidable, but not always

Ravi Varghese, Director, Head of Sustainable Investing, TD Epoch

Anyone who has been part of any sort of organization quickly realizes that conflict is inevitable. Complex goals require scale, which in turn requires multiple people (and often multiple teams) to collaborate to achieve the organization's outcome. Yet these groups often have competing goals and incentives, which can be kindling for organizational strife.

Assessing how well companies balance these competing objectives is a core part of sustainable investing, which we define as the holistic analysis of factors which allow companies to thrive over the long term. Thankfully, these lessons are everywhere. As students of organizational dynamics, we couldn't help but raise an eyebrow when soccer coach Rui Faria, who most famously worked alongside legendary soccer manager Jose Mourinho for 17 years, posted a cryptic message on Instagram1. In the post, Faria criticizes modern football clubs as often prioritizing business objectives over sporting success. He also observes that coaches are presented as leaders of a holistic sporting project, even though their real decision-making power is constrained by departments focused on meeting financial or operational targets. This fragmented, numbers-driven approach undermines team performance, but coaches still bear public responsibility when results and trophies fail to materialize.

Faria has not been involved in competitive soccer since 2020, so internet commentators quickly speculated that the message was aimed at the ownership structure at Manchester United, where Faria was assistant manager from 2016-2018. Manchester United recently parted ways with their head coach, Ruben Amorim, after reported disputes between Amorim and the club's administrative structure. Notably, Faria might just as easily have been referring to another former club, Chelsea, which also released its head coach, Enzo Maresca, under similar circumstances.

For those who are unfamiliar with some of the dynamics in professional soccer, many soccer clubs used to have a manager who supervised a wide range of tasks. Primarily, he would oversee training the team and selecting both tactics and players. However, he would also oversee other responsibilities such as identifying players to transfer into the club and developing youth teams. This role came with immense power, but its broad scope sometimes created upheaval when managers left. As professional soccer has become increasingly competitive (and lucrative), further specialization has occurred. Many clubs have hired sporting directors and/or technical directors to oversee sporting operations. Having more cooks in the kitchen, however, has brought additional complexity. For example, one major source of tension between managers (now often referred to as "head coaches", conveying their reduced role) and sporting directors is player transfers. Most head coaches no longer have main sway over which players are transferred in and out of the club. As the Financial Times2 notes, "to use a corporate analogy, [the head coach] is more departmental head than chief executive."

Faria's comments strike at the heart of this tension and reflect that all organizations suffer from conflict among stakeholders. Mercifully, some of this conflict can be avoided. We believe that strategy and systems are among the most important mechanisms for preventing conflict among internal stakeholders. Specifically, organizations must be aligned on a clear winning aspiration, shared across different units. This winning aspiration must be buttressed by appropriate management systems, particularly systems of accountability and evaluation.

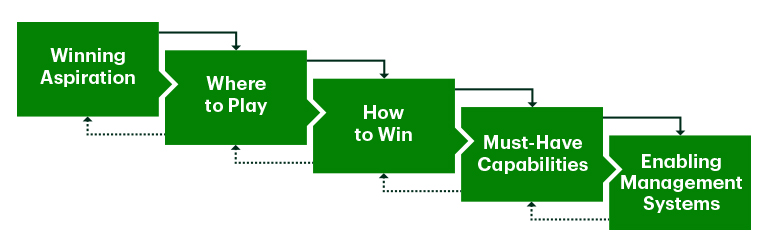

To provide some context, one of our favorite frameworks for thinking about strategy comes from "Playing to Win: How Strategy Really Works", by A.G. Lafley and Roger Martin3, which lays out a series of decisions an organization must make to create and execute a winning strategy.

The very first of these decisions is to align on a winning aspiration. Faria's post calls out the tension between winning silverware and operating within a business plan, with many critics alleging that teams are being run to maximize profits rather than sporting success. We see this dynamic in corporations, too. Bob Lutz, former Vice Chairman of General Motors (GM), famously wrote a book called "Car guys vs. bean counters: The battle for the soul of American business4", in which he lambasted the dominance of the number-crunchers, and advocated giving the reins to the 'product guys'… those with vision and passion for the customers and their product or service. In other words, Lutz was decrying a lack of agreement on what GM's winning aspiration should be. Admittedly, identifying a winning aspiration can be complex, with companies receiving mixed signals from multiple stakeholders. Even a supposedly monolithic group, such as shareholders, can have different views. Should management be asked to grow their top line, maximize free cash flow, earnings per share or returns on capital? Similarly, should the professional soccer team prioritize profitability, winning silverware or entertaining fans? Faria's teams, helmed by Jose Mourinho, won an awful lot but were often criticized for failing to entertain. The devil is in the detail, but an organization that lacks clarity on its winning aspiration is certain to struggle.

We are going to gloss over the decisions on "where to play", "how to win" and "must-have capabilities", but suffice it to say that these are essential components in effective and coherent strategy. The Faria post, however, strikes at the importance of designing management systems. First, alignment and accountability should not be mutually exclusive. Faria is quite right that a winning team is more than the sum of its parts. One of the key tasks of management is to create alignment between various parts of the organization which may occasionally come into conflict. Again, this flows from a clear winning aspiration which is communicated to the entire organization. While Faria is right to criticize misguided individual department objectives, the fact is that individual units need accountability. As Lafley & Martin argue, measurement provides focus and feedback. These lay the groundwork for accountability and rigorous evaluation. Management tools such as combining organizational objectives with measurable key results (OKRs) are explicitly designed to balance alignment with accountability and avoid the situation Faria pinpoints. If individual business units have key performance indicators (KPIs) which are out of sync with broader organizational goals, it is the role of management to set appropriate goals at the unit level.

Faria suggests that coaches are being misled into believing they are in charge of “the project”. In truth, it is no shame for head coaches to be more like a "departmental head" if it leads to better outcomes for a team - assuming this has been effectively communicated to the coach. Alignment on the scope of the prospective coach's authority is essential from the offing in conversations with boards or club owners. Similarly, a corporate board needs to be clear with a chief executive officer (CEO) where their authority ends. The corollary, however, is that the CEO or coach can only be assessed on the results they can conceivably be expected to influence. These are examples of the clear and effective decision-making systems required for organizational excellence.

We are under no illusions: organizational conflict is inevitable. However, a clear winning aspiration and effective management systems can go a long way to prevent some of that conflict. As shareholders who encourage management to run companies for the long term, we vastly prefer to see bitter rivalries being played out on the soccer pitch rather than the corporate arena.

1 Source: https://ca.sports.yahoo.com/news/rui-faria-former-assistant-manager-083000584.html?guccounter=1

2 Source: https://www.ft.com/content/de6f1ea3-1c41-4ba6-9975-69e855cfc65e

3 Lafley, A.G., & Martin, R.L. (2013). Playing to Win: How strategy really works. Harvard Business Review Press.

4 Lutz, R.A. (2011). Car guys vs bean counters: The battle for the soul of American business. Portfolio/Penguin

The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax, accounting or investment advice. Particular investment, tax or trading strategies should be evaluated relative to each individual's objectives and risk tolerance.

This material is not an offer to any person in any jurisdiction where unlawful or unauthorized. These materials have not been reviewed by and are not registered with any securities or other regulatory authority in jurisdictions where we operate.

Any general discussion or opinions contained within these materials regarding securities or market conditions represent our view or the view of the source cited. Unless otherwise indicated, such view is as of the date noted and is subject to change. Information about the portfolio holdings, asset allocation or diversification is historical and is subject to change.

This document may contain forward-looking statements (“FLS”). FLS reflect current expectations and projections about future events and/or outcomes based on data currently available. Such expectations and projections may be incorrect in the future as events which were not anticipated or considered in their formulation may occur and lead to results that differ materially from those expressed or implied. FLS are not guarantees of future performance and reliance on FLS should be avoided.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Any characteristics, guidelines, constraints or other information provided for this material is representative of the investment strategy and is provided for illustrative purposes only. They may change at any time and may differ for a specific account. Each client account is individually managed; actual holdings will vary for each client and there is no guarantee that a particular client's account will have the same characteristics as described herein. Any information about the holdings, asset allocation, or sector diversification is historical and is not an indication of future performance or any future portfolio composition, which will vary. Portfolio holdings are representative of the strategy, are subject to change at any time and are not a recommendation to buy or sell a security. The securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio. It should not be assumed that an investment in these securities or sectors was or will be profitable.

The securities disclosed may or may not be a current investment in any strategy. Any reference to a specific company listed herein does not constitute a recommendation to buy, sell or hold securities of such company, nor does it constitute a recommendation to invest directly in any such company. Any projections, targets, or estimates in this presentation are forward-looking statements and are based on our internal research, analysis, and assumptions. There can be no assurances that such projections, targets, or estimates will occur and the actual results may be materially different. Additional information about our assumptions is available upon request. Other events which were not taken into account in formulating such projections, targets, or estimates may occur and may significantly affect the returns or performance.

For Jurisdictions Outside of Canada and the United States: This information is only intended for use in jurisdictions where its distribution or availability is consistent with local laws or regulations. TD Asset Management Inc. and Epoch Investment Partners, Inc. products are also available through a network of affiliated and unaffiliated distributors. Please contact our distribution partners to find out more.

Australia: Epoch Investment Partners, Inc. (ARBN: 636409320) holds an Australian Financial Services License (AFS License No: 5308587) and is incorporated in Delaware, USA (liability of members is limited). To the extent any statements contained in this document constitute financial product advice, those statements are issued by Epoch Investment Partners, Inc. The information contained herein is intended for wholesale clients and investors only as defined in the Corporations Act of 2001.

Japan: For Japanese residents, please note that if you have received this document from The Toronto-Dominion Bank entities based outside Japan, it is being provided to qualified financial institutions (“QFI”) only under a relevant exemption to the Financial Instruments and Exchange Act.

If you have received this document from TD Securities (Japan) Co., Ltd., it is being provided only to institutional investors. TD Securities (Japan) Co., Ltd. is regulated by the Financial Services Agency of Japan and is distributing this document in Japan as a Type 1 and Type 2 Financial Instruments Business Operator registered with the Kanto Local Finance Bureau under registration number, Kinsho 2992, and a member of Japan Securities Dealers Association.

South Africa: Epoch Investment Partners, Inc. is a licensed Financial Services Provider (license number 46621) with the Financial Sector Conduct Authority. TD Global Investment Solutions represents TD Asset Management Inc. ("TDAM") and Epoch Investment Partners, Inc. ("TD Epoch"). TDAM and TD Epoch are affiliates and wholly owned subsidiaries of The Toronto-Dominion Bank.

New Zealand: This document is not an offer of financial products requiring disclosure under the Financial Markets Conduct Act 2013 (New Zealand). This document is only for “wholesale investors” within the meaning of clause 3(2) of Schedule 1 of the Act and any offer of financial products will only be made to “wholesale investors”. Neither TDAM, TD Epoch, TD Global Investment Solutions nor The Toronto-Dominion Bank are a registered bank in New Zealand.

Additional Disclosure

On September 10, 2025, the Chicago Mercantile Exchange (“CME”) made findings involving The Toronto-Dominion Bank (“TD”) related to a transaction effected on the Chicago Board of Trade (“CBOT”) in June 2023. The CME determined that the transaction was executed in order to transfer a futures position between accounts with common beneficial ownership in violation of CBOT Rules 534 and 538.C. Without admitting or denying any violations or factual findings, TD consented to the entry of findings by the CME and paid a penalty of $25,000. None of the conduct regarding this matter involved Epoch Investment Partners, Inc. or its employees. A copy of the CME findings can be found here: https://www.cmegroup.com/content/dam/cmegroup/notices/disciplinary/2025/09/cbot-24-1744-bc-toronto-dominion-bank-nda-posting.pdf

TD Global Investment Solutions represents TD Asset Management Inc. ("TDAM") and Epoch Investment Partners, Inc. ("TD Epoch"). TDAM operates in Canada and TD Epoch operates in the U.S. Both entities are affiliates and wholly-owned subsidiaries of The Toronto-Dominion Bank. TDAM and TD Epoch products are also available through a network of affiliated and unaffiliated distributors. Please contact our distribution partners to find out more. ®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

Related content

More by this Author