@TDAM_Canada

Investor Knowledge 5 Minutes

In today’s uncertain market environment, low volatility strategies remain a critical tool for investors seeking to preserve capital while maintaining equity exposure. Geopolitical shifts, fluctuating trade policies, and economic uncertainty have fueled volatility, leading to a starkly different market landscape in the first quarter of 2025 compared to the past two years. The year began on the same upward trajectory that closed out 2024, but the "risk-on" rally quickly lost momentum. Markets quickly reversed course as U.S. President Donald Trump’s unpredictable tariff policies triggered "risk-off" sentiment, unsettling global stability.

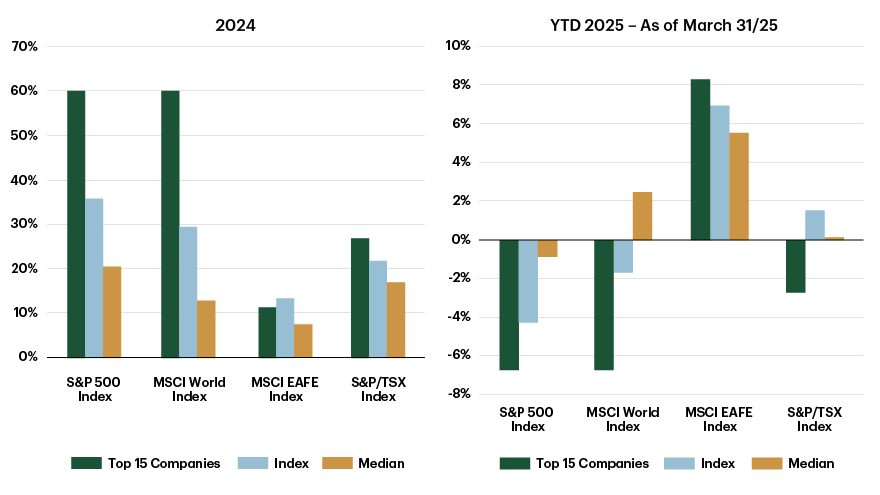

The mega-capitalization (cap) stocks that previously propelled cap-weighted indices higher have now become a drag, pulling markets lower. A notable bright spot has been the Europe, Australasia, and the Far East (EAFE) region, which significantly lagged the U.S. market last year but has so far avoided this year’s downturn, delivering positive year-to-date returns.

Figure 1 – Large-cap players led on the upside in 2024 and the downside in 2025

Source: FactSet Research Systems Inc. As of Mar 31, 2025.

A steady hand

Low volatility strategies have provided a steady hand amid the market turbulence, reinforcing their role in capital preservation during volatile periods, and ultimately delivering a smoother return experience. By capturing a portion of the market’s early-year gains while sidestepping the recent downturn, these strategies have demonstrated resilience in navigating today’s unpredictable market conditions.

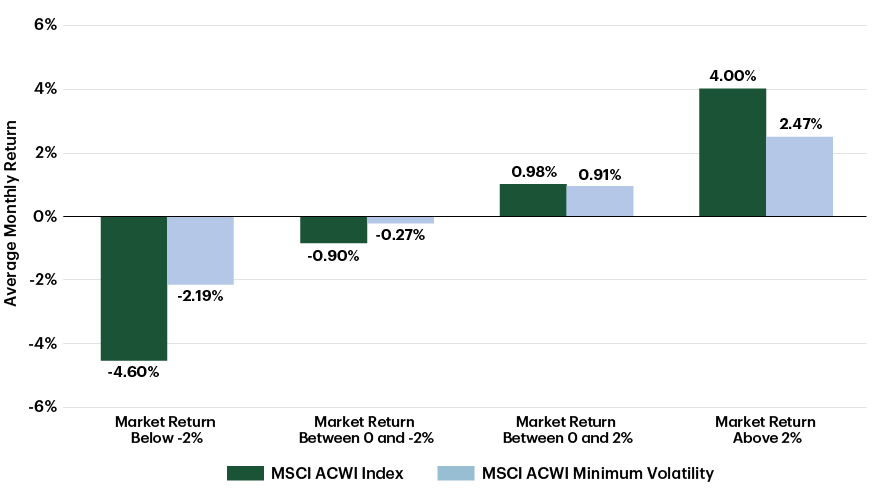

Low volatility strategies primarily invest in stable, non-cyclical companies. Because these strategies are constructed to have less risk than a cap-weighted benchmark with the goal of providing better risk adjusted returns, low volatility strategies will tend to lag in strong upward moving markets as seen in 2024 but provide capital preservation by limiting participation in market declines. Low volatility strategies demonstrated resilience during the 2022 drawdown and again in the brief market correction in the third quarter of 2024. The defensive nature of low volatility is working to the benefit of its investors in 2025 acting as a calm within a volatile storm. Over the long-term investing cycle, low volatility strategies typically generate much of their relative performance in adverse equity markets.

Figure 2 – What to expect in up and down markets for a low volatility investor - An average monthly return comparison

Source: Bloomberg Finance L.P. Data from December 31, 1998 to March 31, 2025

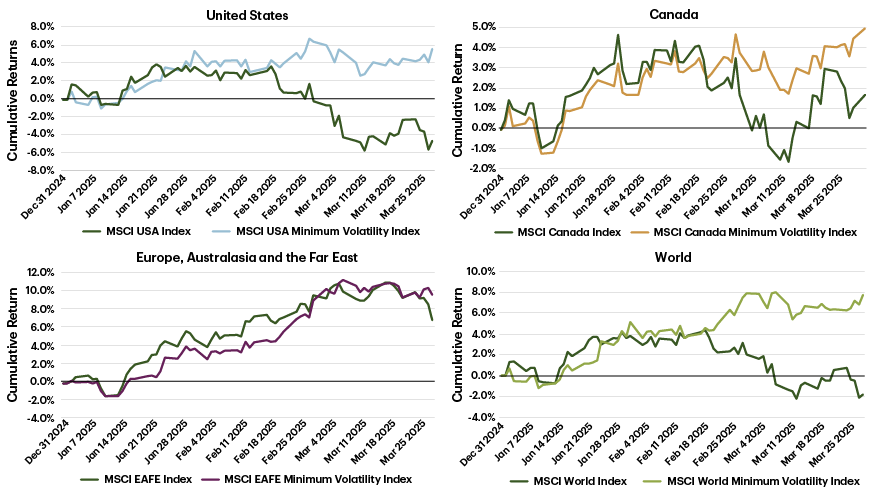

When comparing the year-to-date performance of low volatility strategies to cap-weighted indices globally, it is clear that there has been a shift in sentiment and a move towards a de-risking environment. Low volatility indices are continuing to deliver positive returns while global cap-weighted indices are negative. Future market movements will continue to be impacted by the ever-changing tariff landscape.

Figure 3 – Minimum volatility indices are weathering the tariff storm

Source: Bloomberg Finance L.P. Data from December 31, 2024 to March 31, 2025

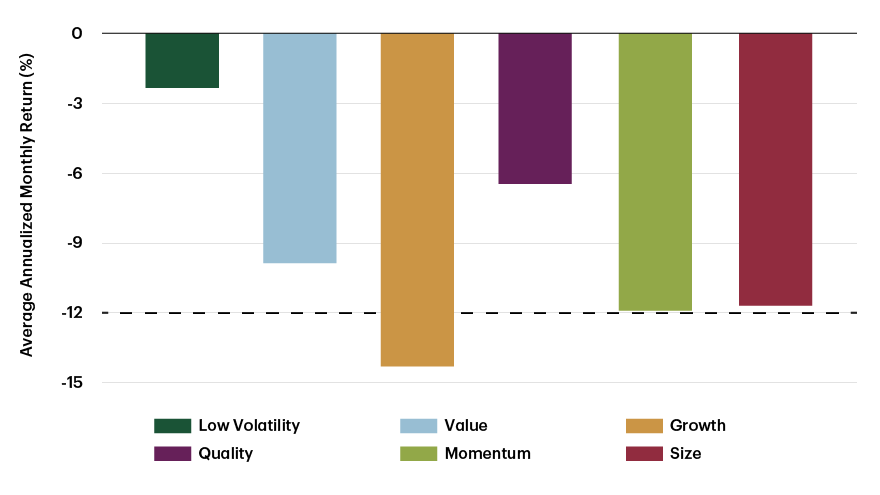

In 2023, the team at TD Asset Management Inc. (TDAM) published an article on de-risking and the downside protection of low volatility. Diversification is a critical tool for reducing risk, yet it is often overlooked until market stress highlights its necessity. Low volatility strategies, by design, have less risk than other equity styles and lower downside correlations. While low volatility is not the top-performing factor all the time, when we average across multiple periods, the low volatility style remains the best alternative for capital preservation and downside portfolio protection within equities, in times of market stress.

Figure 4 – Style performance during crises – Low volatility, on average, provides more capital preservation

Note: Average annualized monthly returns refers to the average annualized return over the 94 months spanning the six crises described here. Source: MSCI, TD Asset Management Inc. As of May 31, 2023.

The certainty of continued uncertainty

The ongoing uncertainty surrounding tariffs, both in terms of scope, implementation, and potential escalation, is contributing to increased market volatility. Historically, such environments have provided an opportunity for low volatility strategies to add value, as they are designed to offer potential downside protection during periods of heightened uncertainty. As tariffs are announced and the likelihood of the application of global reciprocal tariffs increases, broad markets tend to react sharply negative. Given their defensive nature, low volatility strategies will typically experience lower downside participation.

This is exactly what low volatility investors experienced over the two trading days of January 31st and February 1st, when the broad Canadian market dropped more than 2% on the U.S. announcement of initial tariff intentions against Canada and Mexico. Overall, trade tensions and tariff-related disruptions can be detrimental to global growth, but such conditions often reinforce the value of low volatility strategies.

In today’s uncertain market environment, the case for low volatility investing remains compelling. By prioritizing capital preservation and risk-adjusted returns, these strategies help investors remain disciplined through volatile market cycles. While they may lag in strong upward-trending markets, their ability to cushion against sharp downturns has historically led to better long-term risk adjusted performance. With geopolitical shifts, international trade disputes, and economic uncertainty continuing to weigh on investor sentiment, low volatility strategies can be the calm within the storm and serve as an essential tool for managing risk while maintaining equity exposure. As history has shown, market downturns are inevitable, and having a strategic allocation to low volatility can help investors navigate uncertainty while still participating in long-term growth opportunities.

The information contained herein has been provided by TD Asset Management Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

Bloomberg and Bloomberg.com are trademarks and service marks of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries. All rights reserved.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto Dominion Bank or its subsidiaries.

TDAM Connections at a Glance:

You might also be interested in:

TDAM Talks Podcast

A Look Into Our Best Thinking

Explore our Insights