@TDAM_Canada

Market Perspectives 10 Minutes

Now that we know what "Liberation Day" has brought in terms of the magnitude and breadth of tariffs being unleashed on America's allies and trading partners, the unknown that remains is duration – how long will this economic tremor last? The longer these measures are in place, the more disruptive and destructive these policies will likely be on the global economy. Any "adjustments" made by corporations to re-align supply chains could take years, if not decades, to establish, while consumer patterns and behaviours may potentially be impacted for a generation.

In an environment of rapidly changing policies, reciprocal responses, and further "deals" to be negotiated, the TD Asset Management Inc., Asset Allocation Team ("we, "the team") have been preparing for a range of potential scenarios since early 2024, when the leading presidential candidates were finalized, and policies were announced. To be candid, there was hope for a more measured and prudent approach to any perceived trade imbalances, in hopes that those with "cooler heads" in the administration would prevail. Nevertheless, countries and markets have responded accordingly, and we are also monitoring in real time key developments that may shape returns and risks going forward.

The global market sell-off following U.S. President Donald Trump’s tariff announcement on April 2 has rattled investors, with overseas markets and the S&P 500 Index all ending lower for the week. The S&P 500 Index is almost 20% below the mid-February all-time high (as at April 4). As at the time of writing, countermeasures to U.S. tariffs are emerging, with Canada announcing 25% tariffs on certain U.S. vehicles on April 3, while China will reportedly place an additional 34% tariff on all U.S. imports beginning Thursday April, 9. In Europe, French President Emmanuel Macron urged corporations to halt spending in the U.S. U.S. President Trump said he would consider reducing tariffs in return for countries offering something “phenomenal” to the U.S., though also suggested that sector tariffs on pharmaceuticals and semiconductors could be announced soon. Bond yields have fallen sharply lower, with both the U.S. and German 10-year nominal yields down around 15 basis points ("bps") to 3.88% and 2.50%, respectively. U.S. Federal Reserve Chair Jerome Powell spoke on Friday, and while not reacting with any monetary action, acknowledged the inflation threat of tariffs in the committee's forecasts. Market volatility has pushed the Volatility Index ("VIX") to 41, the highest since the growth scare in the summer of 2024, while U.S. high-yield credit spreads, a gauge of global risk premia, jumped by more than 50bps on April 3, the largest rise since March 2020.

Market Expectations and Outlook

Early estimates from economists highlight that the latest U.S. tariff measures could lower global Gross Domestic Product ("GDP") growth by at least 50bps, with a potential 100 to 150bps drag to U.S. GDP growth, a 100bps drag to China and a 40 to 60bps hit to Eurozone GDP growth. This comes against the backdrop of U.S. growth that has already started to weaken recently on the back of softening consumer spending. For global PMI, there is a potential 3 to 4 point downside risk due to tariffs. Three years of strong global growth left asset prices high, risk premia compressed, and earnings expectations elevated. Even before the latest tariff shock, the global growth outlook had started to darken, given the weakening run-rate of U.S. growth and the unexpected shift in U.S. policy focus from tax cuts to spending cuts. This had already led the MSCI World Index to decline by 6% from its all-time high and U.S. high-yield credit spreads, a good gauge of global risk premia, to rise by 80bps from a 17-year low.

Positioning

We continue to believe it is prudent to be on top of policy shifts from the current U.S. administration. As a result of this fluid policy dynamic, we maintain the ability to be tactical and nimble within TDAM investment portfolios in the current environment as we lean into alternative sources of diversification.

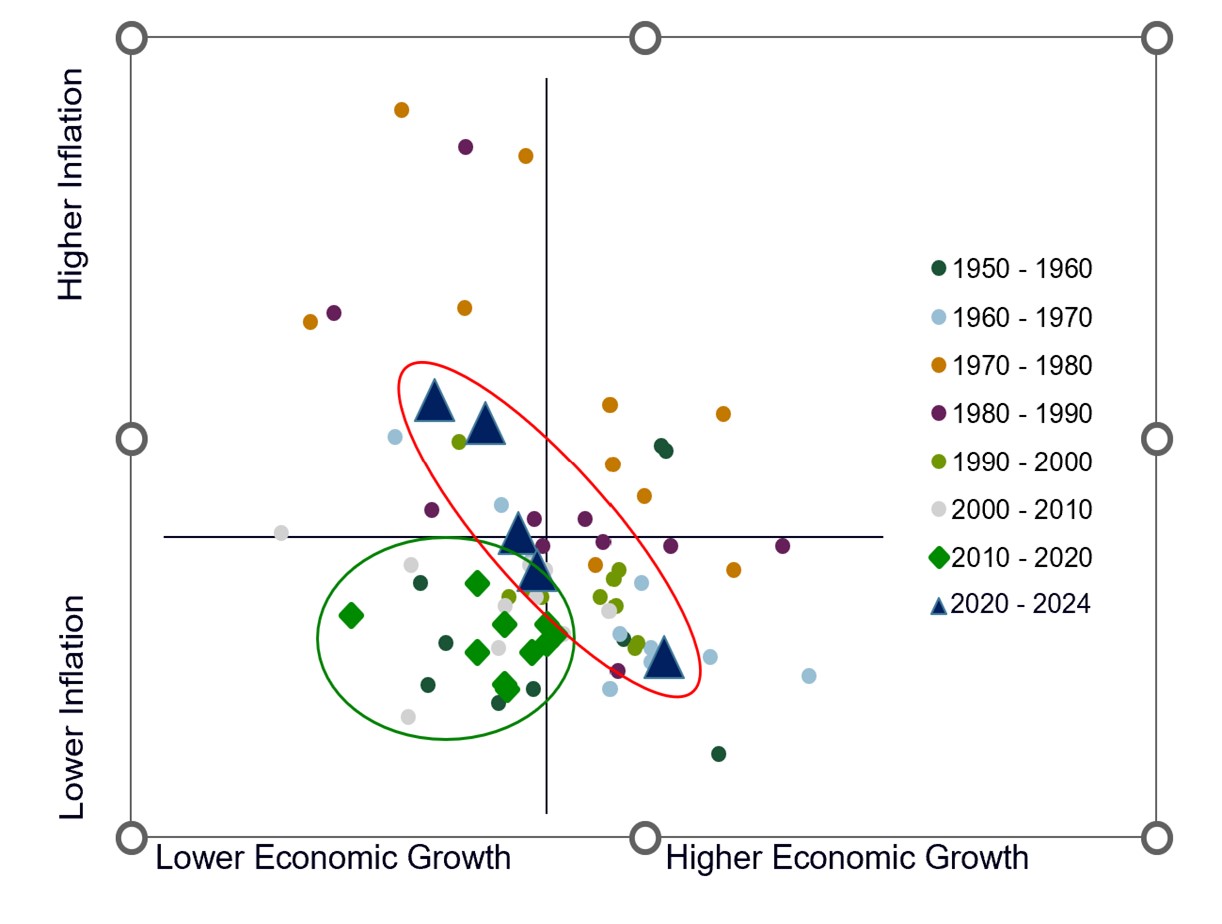

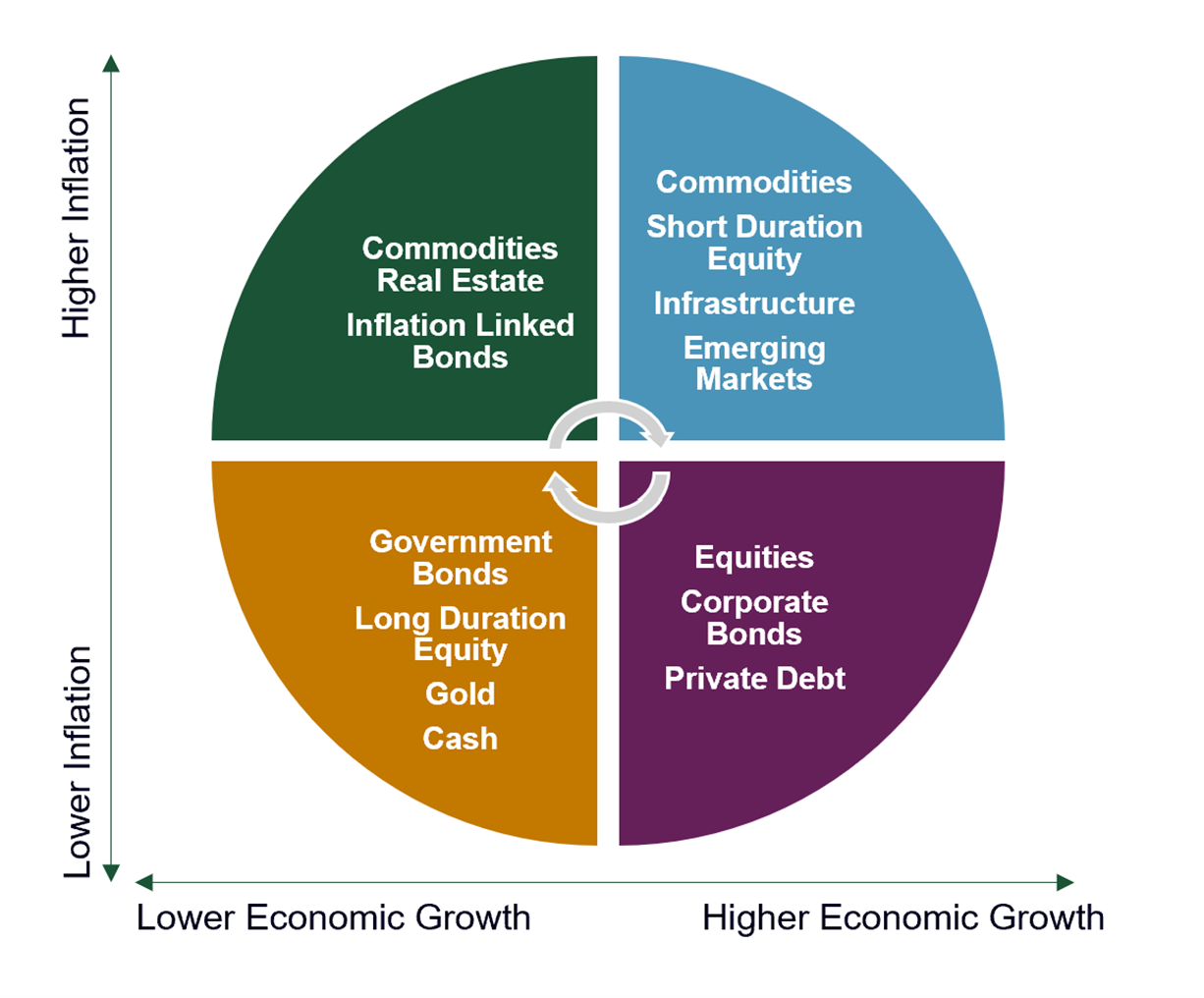

As we have outlined before, changes in investment regime have occurred more rapidly in the last decade than ever in recent history. As a result of the COVID-19 pandemic, hyperinflation, and now tariff tremours, we have shifted through several quadrants of growth/inflation. High degrees of macroeconomic uncertainty, especially concerning policy, can lead to periods of weakness for financial assets, but to varying degrees. Assets perform differently in diverse environments, and in the current climate of uncertainty, the best approach, in our view, is to maintain a diversified portfolio of non-correlated assets as your best defense.

Actively invest in a broader toolkit as non-traditional assets can mitigate risk/volatility

In this current environment, we have remained prudent in maximizing tactical flexibility and sources of diversification across all of our asset allocation portfolios, subject to distinct product/benchmark constraints. We have taken advantage of recent market volatility to add to positions where we feel there is relatively more risk-adjusted return potential and more stability. Here are some general examples of recent trades that have been implemented in anticipation of near-term uncertainty.

Fixed Income:

- Within the TD Fixed Income Pool, we are collecting higher yields than the benchmark through higher-quality credit and mortgages and are currently neutral to slight underweight duration

- We have continued to reduce longer-duration government bonds tactically.

- Re-allocated to high-quality corporate credit bonds, offering higher yields and limited downside risk.

- Added to private credit and mortgages for differentiated sources of income with low duration.

Equities:

- We have already continued to diversify away from the U.S. since the end of 2024, particularly decreasing weight in U.S. Technology sector stocks towards other regions and quality-factor equities.

- We increased to a neutral weighting towards Canadian banks by adding to Canadian Exchange Traded Funds (ETF) last fall. Canadian banks have performed strongly as fundamentals were better than analysts feared and benefitted from the flight to dividend payors. Canadian equity and economic performance have been improving, despite trade war headwinds. There is a possibility of improving U.S.-Canada relations and an investment in our nation's productivity and growth following a Canadian election, which could be positive for key Canadian sectors.

- We have been allocating more to targeted European ETFs due to rising tailwinds from fiscal spending, a strong Financials sector, low valuations, strong earnings, and a potential resolution to the Ukraine war. However, this reallocation has been measured, given Europe's high sensitivity to tariffs, and near-term investor sentiment has pushed valuations upwards quickly. We continue to believe that regional diversification is prudent as many investors globally are overly concentrated in the U.S.

- On a sector basis, we maintain a balanced allocation, with an overweight stance toward the Financials, Technology, Discretionary, Health Care and Industrials sectors.

- We believe the market may remain choppy and range-bound as policy uncertainty is digested. We will be pacing the deployment of remaining cash into equities as the market works through the current turmoil, particularly in quality names that may have been arbitrarily oversold along with the rest of the market.

Alternatives:

- We expect to increase our allocation to Infrastructure over the next 3 months as further capital calls for deals continue.

- We have increased the allocation to the commodity strategy and toward gold equities as the underlying commodity price has reflected a flight to safety.

The information contained herein has been provided by TD Asset Management Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual's objectives and risk tolerance.

Commissions, management fees and expenses all may be associated with mutual fund and/or exchange- traded fund ("ETF") investments (collectively, "the Funds"). Trailing commissions may be associated with mutual fund investments. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns. Please read the fund facts or summary documents and the prospectus, which contain detailed investment information, before investing in the Funds. The indicated rates of return (other than for money market funds) are the historical total returns for the period, compounded for mutual funds, including changes in unit value and reinvestment of distributions. The indicated rate of return for each money market fund is an annualized historical yield based on the seven- day period ended as indicated and annualized in the case of effective yield by compounding the seven day return and does not represent an actual one year return. Index returns do not represent ETF returns. The indicated rates of return do not take into account sales, redemption, commission charges, distribution or optional charges, as applicable, or income taxes payable by any securityholder that would have reduced returns. The Funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated.

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

TDAM Connections at a Glance:

You might also be interested in:

TDAM Talks Podcast

A Look Into Our Best Thinking

Explore our Insights