Canada

Canada

US

US

You are now leaving our website and entering a third-party website over which we have no control.

Highlights

SECURITIES AND INVESTMENTS |

|||

NOT A DEPOSIT |

NOT FDIC-INSURED |

NOT BANK GUARANTEED |

MAY LOSE VALUE |

Quarterly Highlights

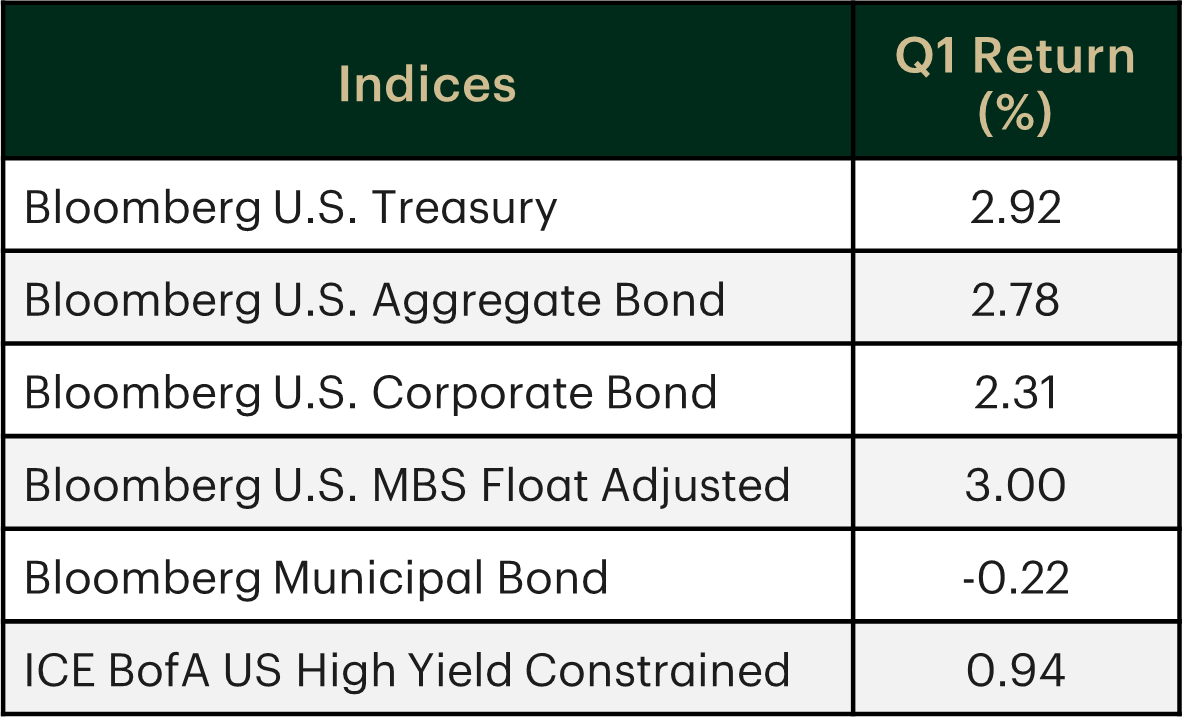

Fixed Income:

- The Bloomberg U.S. Aggregate Bond Index advanced by 2.78% in Q1

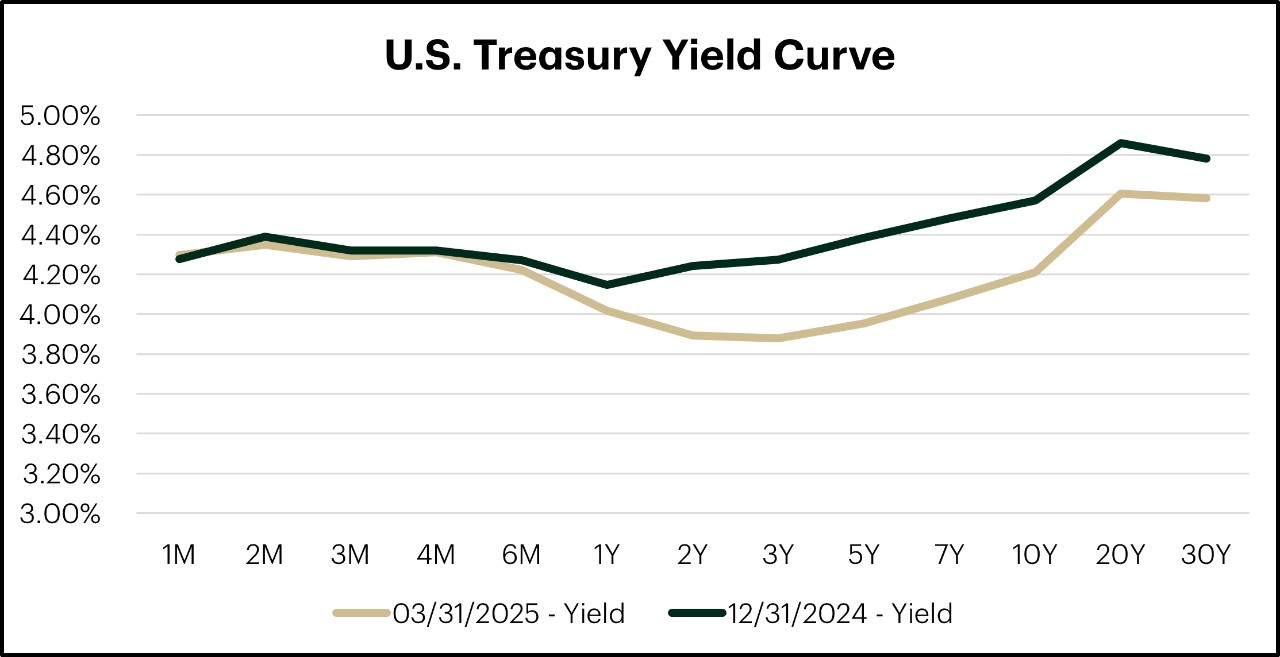

- Treasury prices increased as yields moved lower

- The 10-year Treasury yield declined 36 basis points (bps) to 4.21%, while the 2-year Treasury yield fell 35 bps to 3.89%

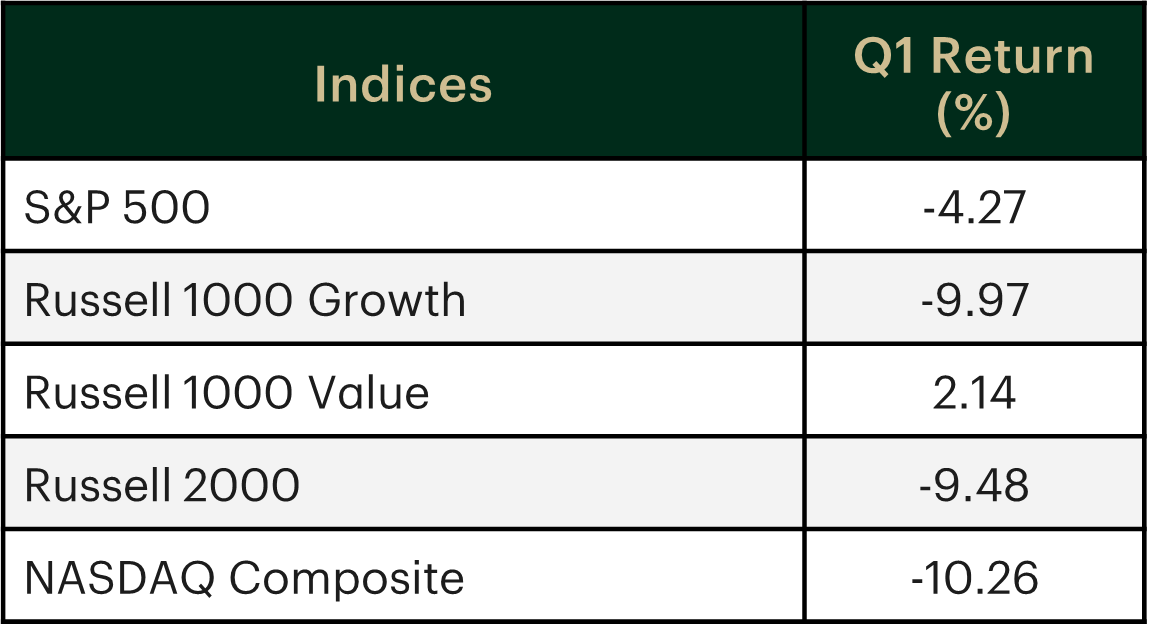

U.S. Equities:

- The S&P 500 Index fell 4.27% in the first quarter, while the technology-heavy Nasdaq Composite Index posted a sharper decline of 10.26%

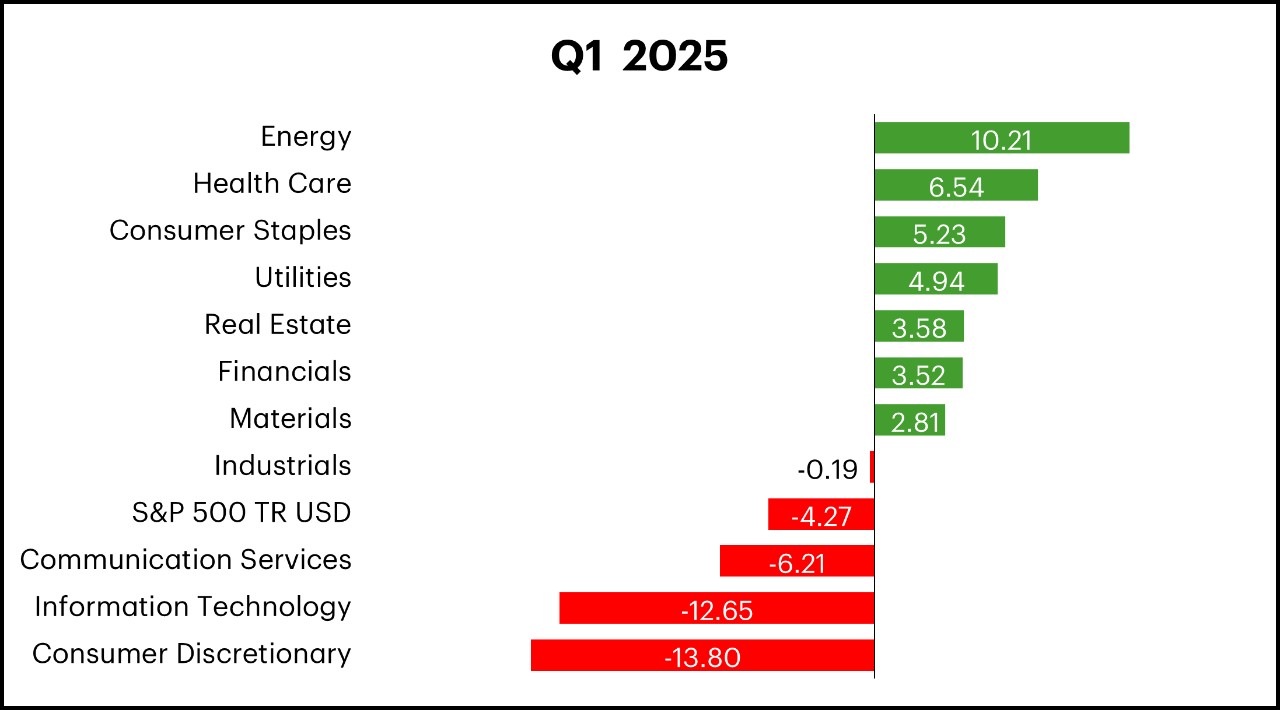

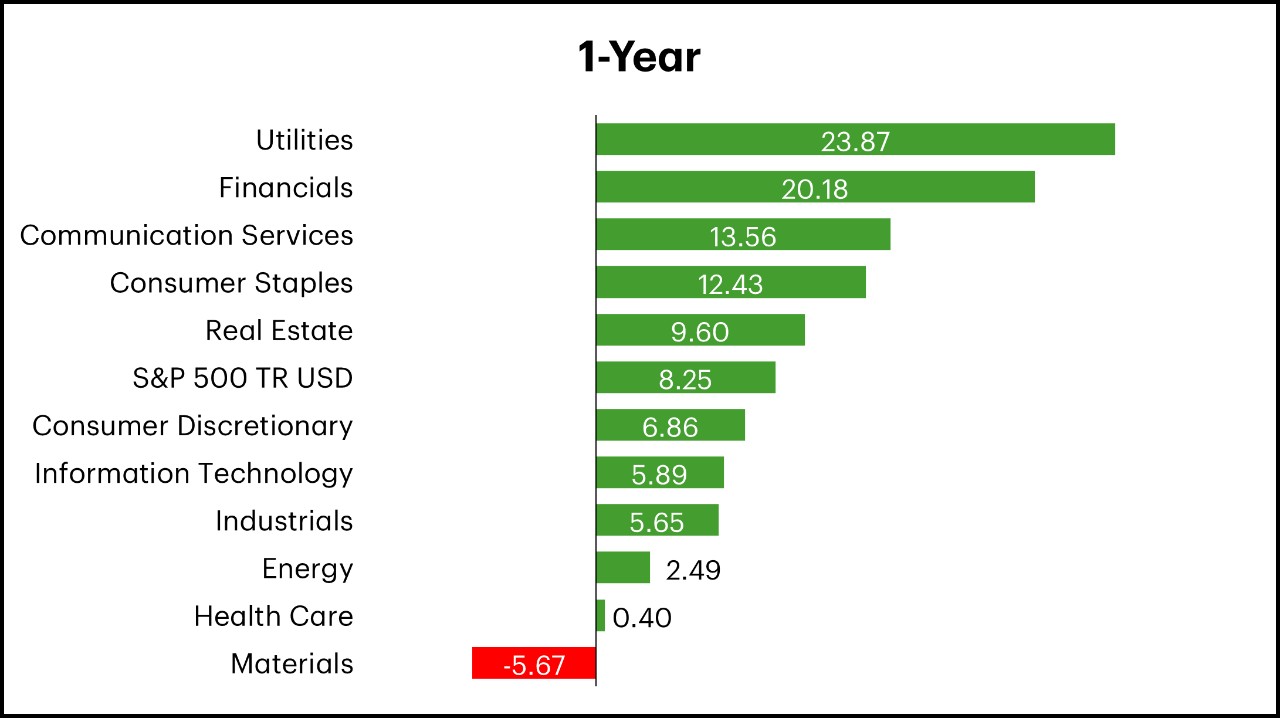

- Seven of the 11 sectors in the S&P 500 Index produced a positive return. The consumer discretionary sector was the weakest

- Large-cap stocks held up better than small-cap stocks, and value stocks registered a gain, outperforming growth stocks

International Stocks:

- International developed and emerging markets generally outperformed their U.S. peers during the quarter

Source: Morningstar Direct as of March 31, 2025, TD Wealth Chief Investment Office. Returns are presented on a total return basis.

U.S. fixed income markets rebounded in Q1, primarily due to a decline in government yields. The drop in yields reflected growing concerns over the economy and heighted uncertainty surrounding President Trump's "2.0 agenda," which led to a flight to safety in Treasuries. The 2-year Treasury yield fell by 35 bps to 3.89%, while the 10-year yield declined 36 bps to 4.21%. The spread between 2-year and 10-year Treasuries remained in positive territory at 32 bps.

The Federal Reserve (Fed) held its policy rate unchanged in the first quarter. In the press conference following the March meeting, Chair Jerome Powell acknowledged the high degree of uncertainty from President Trump’s policy changes but reiterated that the Fed is in no rush to adjust interest rates. He said officials can wait for greater clarity on the effects of these policies on the economy before acting. March economic projections showed a reduction in growth forecasts for this year and an increase in inflation estimates. Officials expect a total of 50 bps in rate cuts this year, implying two quarter-point reductions. The longer-term terminal rate was kept unchanged.

Declining yields boosted performance with the broad U.S. bond market, as measured by the Bloomberg Aggregate Bond Index, finishing the quarter higher by 2.78%. Short-term Treasuries delivered positive performance; however, they underperformed intermediate and longer-term Treasuries. Credit spreads widened modestly in both investment-grade and high-yield corporate bonds, though elevated coupons helped support total returns. Municipal bonds underperformed Treasuries and ended the quarter modestly lower due to a challenging technical environment. Heavy supply weighed on municipal bond prices as demand slowed towards the end of the quarter.

Yield Curve Moves Lower on Growth Concerns, Policy Uncertainty, and Risk-Off Sentiment

Source: FactSet as of March 31, 2025, TD Wealth Chief Investment Office.

Please see Important Information

Source: Morningstar Direct as of March 31, 2025, TD Wealth Chief Investment Office.

U.S. stocks suffered a correction in the first quarter as investors began to price in the strong likelihood that President Trump’s tough talk on trade may amount to more than just a negotiating tactic. Concerns over a potential global trade war outweighed, at least in the short term, optimism around the administration's pro-growth policies.

Early in the quarter, the S&P 500 Index had scaled new heights, driven by investor enthusiasm about the new administration. The brief rally was interrupted by news of a breakthrough in Artificial Intelligence (AI) from China’s DeepSeek. Reports of its ultra-efficient model sparked concerns about U.S. technology dominance and accelerated the rotation away from the big U.S. technology names.

As February progressed, the market regained a tentative footing. The Trump administration showed a willingness to negotiate on trade, pausing North American tariffs after Mexico and Canada vowed to tighten border security. This partial reprieve calmed nerves until later in February, when the president unveiled his plan to impose reciprocal tariffs on trading partners by early April. Prior delays and hopes for negotiation gave way to hard deadlines, and America’s top trading partners braced for impact. As the quarter came to a close, the administration announced stunning 25% tariffs on imported vehicles, which sent equity markets into another tailspin.

For the three months ended March 31, 2025, the S&P 500 Index declined by 4.27% and the Nasdaq Composite Index fell sharply by 10.26%. Seven of the 11 sectors in the S&P 500 Index performed positively. The consumer discretionary sector was the weakest, falling 13.80%. Value stocks (Russell 1000 Value Index) registered a return of 2.14%, outperforming growth stocks (Russell 1000 Growth Index), which fell by 9.97%. Lastly, small-caps fell 9.48%, underperforming large-cap stocks.

S&P 500 Index – Sector Returns (%)

Source: Morningstar Direct as of March 31, 2025, TD Wealth Chief Investment Office. Returns to be presented on a total return basis.

Please see Important Information

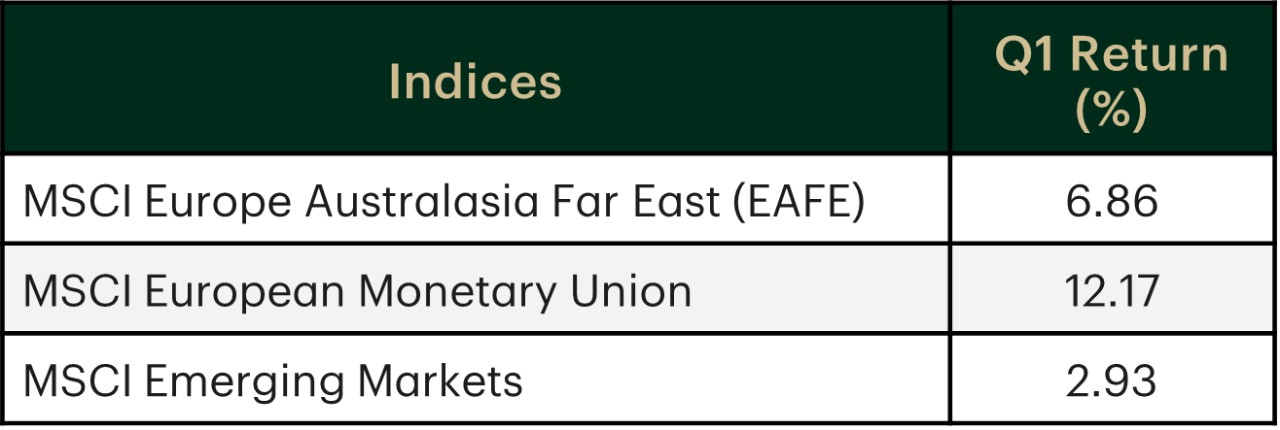

Source: Morningstar Direct as of March 31, 2025, TD Wealth Chief Investment Office. Returns are presented as net index returns. Index returns calculated in U.S. dollars.

International developed equity markets diverged in Q1, with European markets rising sharply and Japanese markets plunging. The U.S. dollar weakened 3.94% over the quarter (relative to a basket of major currencies), amplifying the general outperformance of international equities when reported in U.S. dollar terms.

In the euro area, markets climbed steadily from year-end through early March, supported by divergence in monetary policy. While the Fed held off on further rate cuts, cooling inflation in Europe led the central bank there to cut its policy rate twice in the quarter. Additionally, Germany's historic fiscal overhaul and the rotation away from U.S. tech stocks into more attractively valued European equities helped lift the MSCI European Monetary Union Index. The Index reached record highs by late February and ended the quarter up 7.56% in local currency.

Japanese markets, after a couple of stellar quarters last year, reversed course in Q1, with the Nikkei 225 plunging 10.08% in local currency. The yen also rose 5.09% against the U.S. dollar, further dampening returns. Japanese equities came under pressure from two key headwinds: (1) the escalating trade war with the U.S. and (2) rising interest rates in Japan.

Emerging markets recovered after a very weak fourth quarter, outperforming U.S. equities but underperforming European markets. The MSCI Emerging Markets Index rose 2.65% in local currency terms. China was a notable outperformer, with the MSCI China Index surging 14.99% (local currency), supported by Beijing's renewed commitment to the technology sector and promises of fiscal and monetary support for the broader economy. A key catalyst was the AI breakthrough from DeepSeek, which helped turn around what had been a relatively poor start to the year for China's equity markets.

Please see Important Information

Connect with a TD Wealth Advisor

Our TD Wealth Advisors are available for a consultation to start planning for your future.