You are now leaving our website and entering a third-party website over which we have no control.

SECURITIES AND INVESTMENTS | ||||

NOT A DEPOSIT | NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE | |

Planning for Uncertainty

In times of uncertainty, the fear of making the wrong decision can lead to inaction. However, the best way to deal with uncertainty is to take a step back, construct a well thought out investment plan, and make incremental adjustments as new information evolves. Focusing on your plan and long-term goals can help to set you up for success while providing the peace of mind that you are on the right track.

In this edition of Perspectives, we explore a number of important topics intended to help you navigate areas where uncertainty may be prevalent. First, we reflect on the key events that shaped financial markets in the first quarter of 2025. Next, our TD Wealth Asset Allocation Committee (WAAC) examines how evolving trade policies and geopolitical shifts are reshaping global markets and what it could mean for investors.

In our final article, TD Wealth Strategist and Goals Based Leader, Mark Hasenauer, focuses on financial planning for individuals with special needs, outlining key considerations to help ensure long-term stability and security.

The key to navigating uncertainty with confidence is having the right information and a clear plan. TD Wealth is here to help keep you informed and well prepared, so you can better position your portfolio to navigate challenges with confidence and resilience.

Anita Mahadeo, CFA, CAIA

Senior Investment Strategist, TD U.S. Wealth Chief Investment Office

The new year started strong for both risk assets and the economy, driving domestic equity markets to reach for fresh heights in the opening months of 2025. Expectations for pro-growth policies from the new administration, including deregulation and tax cuts, extended investor optimism as U.S. equities achieved record all-time highs by mid-February. Tariff talk, however, rapidly changed market dynamics and upended the stock market rally. While the economy continued to move forward at a steady pace, trade related uncertainty has led to a cautious consumer and elevated inflation risk.

The opening quarter of 2025 also proved volatile as all major U.S. equity indices ended lower, with the S&P 500 Index down 4.3% and technology-heavy Nasdaq Composite Index falling 10.3%. Contributing to investor uncertainty was Chinese technology startup DeepSeek, whose introduction of a low-cost Artificial Intelligence (AI) model rattled markets early in the quarter. Reports suggested the low-cost model may perform in line with technology developed by U.S. industry leader OpenAI and that China may be closing the gap in the AI arms race much faster than anticipated. This quickly weighed on markets as investors began to question the high valuations of leading mega-cap technology companies.

The sell-off proved to be short-lived as markets rebounded in mid-February after the Trump administration paused tariffs on key trading partners, Canada and Mexico, helping to calm investor nerves. Only weeks later, the S&P 500 Index briefly experienced its first 10% correction in two years as heightened trade tensions curbed investor's outlook on valuations and growth. While technology-focused companies led domestic equities lower, international markets continued to benefit from a broader set of exposures and relatively modest valuation levels. A softening U.S. dollar magnified the gains from international investments when reported in U.S. dollar terms.

The move to safe haven assets was beneficial for some assets over the quarter including the price of gold, which hit record highs. The precious metal gained 19% in the first quarter, its best quarterly return in decades. For fixed income investors, bonds proved their worth over the quarter, providing some stability in the face of falling domestic equities. Treasury and high-quality corporate bonds were broadly higher over the period while below investment grade bonds provided more muted gains as interest rates largely fell across the curve. Municipal bonds failed to keep pace with their taxable counterparts as a supply/demand imbalance weighed on prices. For their part, the Federal Reserve (Fed) kept their benchmark rate unchanged after cutting twice at the end of 2024. The Fed did note uncertainty surrounding the outlook, lowering their expectations for economic growth and raising the view on inflation. The Fed awaits further clarity on the path of the economy and remains in no rush to make a change to their policy.

As we move into the second quarter of the year, the outlook has been clouded by recent events and the flight to safety continues. Uncertainty is expected to remain elevated into the near future and market participants will continue to assess changing policy, the implications of which are expected to be sizeable and wide ranging. Maintaining a diversified portfolio may provide some level of protection during these challenging times and help investors remain anchored to their longer-term goals.

Major Market Index Returns (Based in USD)

Source: Morningstar Direct as of March 31, 2025. Returns are presented on a total return basis. Returns greater than 1-year are annualized.

Kevin Hebner, PhD

Managing Director, Global Investment Strategist, TD Epoch Member of the TD Wealth Asset Allocation Committee

President Donald Trump is often portrayed as mercurial and transactional, but his economic policy framework flows from two principles that he has held for well over a decade. For a start, he believes America is engaged in Cold War 2.0 and it requires the same trifecta of attributes that proved critical against the Soviet Union: economic strength, technological leadership, and superior defense capabilities.

More controversially, Trump maintains America has been too magnanimous in providing countries with access to the American consumer and the country's defense umbrella. He believes admittance to the U.S. market should be conditional on a level playing field and balanced bilateral trade, otherwise tariffs are justified. Similarly for defense, where presidents since Dwight D. Eisenhower have complained that most North Atlantic Treaty Organization ("NATO") countries are free riding on American mettle.

Four Reasons Why Trump Loves Tariffs

- Trump has described tariffs as his favorite, the most beautiful word in the dictionary. Trump’s first rationale is that he has unilateral power with enormous discretion, so he can enact tariffs quickly. This differentiates from other more conventional forms of industrial policy which are often more efficient from an economics perspective but requires working with Congress.

- Second, just the threat of tariffs provides Trump with a great deal of bargaining power to negotiate on both trade and non-trade issues (it also produces some terrific photo ops, usually at Mar-a-Lago). He used this approach recently with Canada and Mexico to emphasize illegal immigration and fentanyl smuggling. With European Union ("EU") countries, Trump highlights NATO spending arrears. While this approach has produced some middling concessions from allies, it has been much less successful with adversaries such as China.

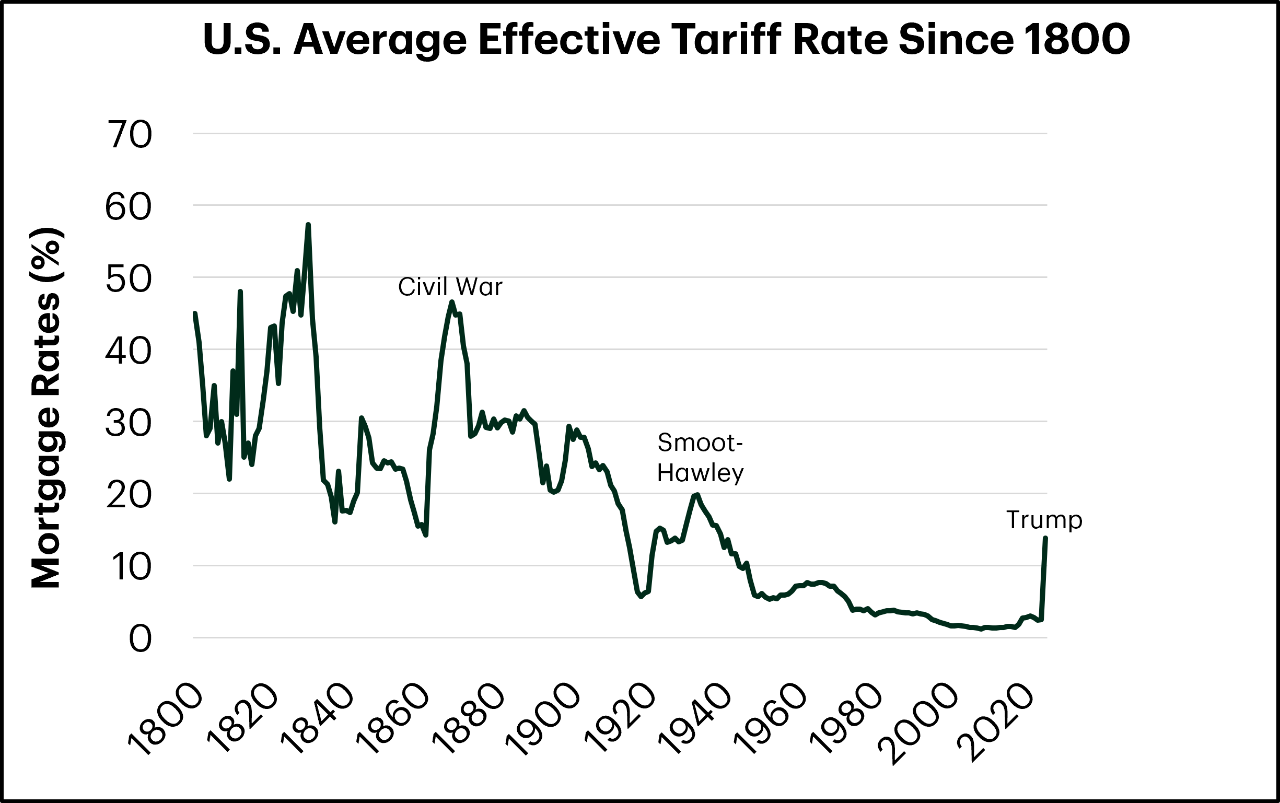

- Next, tariff revenues could plausibly add $80 billion (bn) to government coffers this year. From the founding of the nation until the American civil war, tariffs were typically above 20% and raised roughly 90% of the federal government’s revenue (Figure 1). During the youth of America, a tariff was simply the only tax it had the capacity to enforce.

- Trump’s fourth reason for loving tariffs is they could help restore America’s manufacturing base. He believes the U.S. needs tariffs to prevent a tsunami of subsidized Chinese exports from continuing to hollow out critical sectors. Tariffs could also incentivize homeshoring of investment, production, and jobs. When Trump talks about homeshoring, he has one particular country in mind, and that is China.

Figure 1: U.S. Average Effective Tariff Rate

Source: Bloomberg Finance L.P., Bicentennial Edition: Historical Statistics of the United States, Colonial Times to 1970, United States Census Bureau.

Global Trade War: Is 80% About China

China's economic model is incompatible with the post-Cold War global trading system. That is, its extreme form of mercantilism and belief in one-way trade, is unsustainable and has resulted in enormous backlash from its export markets. The objective is for China to become the #1 global manufacturing powerhouse and to dominate the industries of the future (such as Electric Vehicles, batteries, drones, and robots).

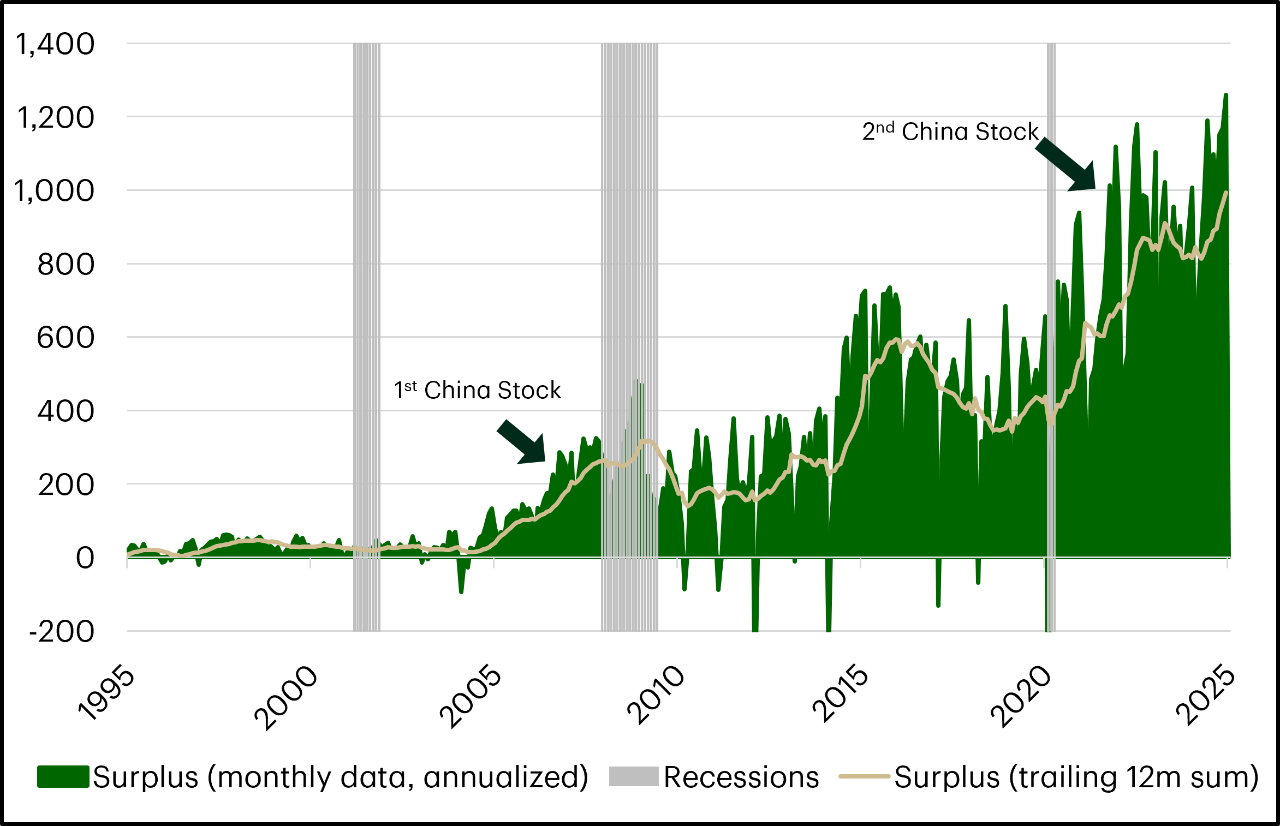

This is manifest in China’s massive trade surplus, with a run rate of over one trillion U.S. dollars ("USD") (Figure 2). This surplus has more than doubled from its pre-COVID-19 level, which was already the largest experienced anywhere in history. To illustrate, Chinese companies now produce 90% of the world’s solar panels, 70% of its batteries and 90% of consumer drones. China also produces more than 50% of the world's aluminum, steel, and ships. Further, during the last three years car exports have tripled, with China becoming the world’s largest car exporter by units. No one in Beijing should be surprised that their export strategy is facing significant challenges, including trade barriers, outright bans, and the threat of much higher tariffs.

Figure 2: China Goods Surplus (USD bn), to Infinity and Beyond

Source: Bloomberg Finance L.P., as at March 6, 2025

The New Global Economic Order

With the rise of China, we have moved from a unipolar to a bipolar world. And in this new world order, China is challenging the U.S. in all three domains of power – economic strength, technological prowess, and defense capabilities.

One implication of the new bipolar order is that the two economic behemoths view interdependence as a risk to both global supply chains and national security. This especially applies to semiconductors, energy, the Electric Vehicle supply chain, and critical medical supplies, as well as the defense industry. For the U.S., the new global economic order features a much more expansive and intrusive role for the state. This includes an active industrial policy, including tariffs, to reduce supply chain vulnerabilities and promote national security and resilience.

Trade War: Implications For Investors

The trade war will remain an important market driver through at least 2028. However, we should be careful about analyzing the impact of tariffs in isolation. Trump's overall policy agenda is pro-growth, emphasizing technology, deregulation, and tax cuts. However, the timing of these policies remains unclear.

We expect a more expansive role for the state, driven by national security concerns rather than economics and efficiency. Tariffs and other forms of industrial policy will be used to reduce chokepoints and vulnerabilities, especially in sectors such as semiconductors, energy, critical minerals, medical supplies, shipbuilding, and defense.

Given the elevated level of uncertainty it is important that investors diversify and avoid becoming overly concentrated in the Magnificent 7 stocks, for example, U.S. equities, or the USD. Correlations across regional equity markets are currently the lowest in 30 years, which makes it an especially opportune time to diversify.

Mark Hasenauer

Wealth Strategist & Goals Based Advice Leader (US)

According to the United States Census Bureau, estimates indicate over 44 million individuals (over 13% of the U.S. population) have a disability.

This article will touch on some of the considerations that exist when putting a plan in place for an individual with special needs.

FOR INFORMATIONAL AND EDUCATIONAL PURPOSES ONLY.

Cash Flow Considerations

A good place to start is the cash flow considerations necessary for the long‐term success of a plan. The fundamental elements of a cash flow plan are identifying: (i) anticipated living and medical expenses; (ii) what income sources are in place and whether additional assets are required to supplement the income sources; and (iii) how long will the assets last given the likely costs and expenses. This will allow you to begin planning now to make sure the required assets are available both today and in the future.

Next you may want to consider scenarios to stress test your plan. What if the costs of care were to increase? What if something were to happen to the primary caretaker or a source of financial support provided by a family member ceased? This might occur when a parent or other financial sponsor becomes disabled, loses capacity with age, or passes away. An individual may also lose access to government funding or programs. How does this change the probability of success for the cash flow plan? What contingencies can be put in place to make sure the plan still works?

The plan is a living document and should be revisited periodically, not only to make sure that it remains relevant under existing circumstances, but also as a tool to help make decisions when substantive changes are being considered regarding investment strategy and spending goals.

Asset Protection Considerations

Another important consideration is to not disqualify the individual for public benefits that are essential for the continued success of their plan. Understanding the rules of qualifying for public benefits in the state where the individual resides is an important part of the planning process.

Transferring assets without restriction to the individual may have a substantial impact on their ability to receive essential

public benefits. These benefits often come from Medicaid and Supplemental Security Income (SSI). Depending on the availability of assets or income, the individual may be rendered ineligible for SSI and Medicaid. Some of the lost benefits may include assisted housing, employment assistance, medical assistance, personal care aides, and transportation assistance.

In planning for the continued receipt of public benefits, one option that may be considered is leaving assets to other family members. This is usually done with the understanding that the other family members will take the individual's needs into consideration. One issue with leaving assets to others is that there may be no formal plan for the benefit of the special needs individual. What if that other family member were to suffer from incapacity, disability, or death? What if the assets become subject to creditor claims or divorce? What if the caretaker's subsequent decisions are not in line with your goals or the needs of the individual being planned for? Or what if the entrusted family member mismanages the funds even with good intentions?

One strategy to address these questions is to leave assets to a Supplemental Needs Trust (SNT). A SNT is designed to provide access to trust owned assets that will not otherwise disqualify a beneficiary from receiving public benefits that are available based on their needs and income levels. The trust must follow requirements regarding continued qualification for these benefits.

Additionally, an SNT may be considered a first or third‐party trust. A self‐settled SNT created by the beneficiary is considered a first party trust, while a trust created and funded by someone other than the beneficiary is considered a third‐party trust. There are different rules regarding each of these trusts. It is important to consult with a qualified attorney who has experience in drafting SNTs to make sure that it is drafted appropriately based on the individual circumstances of the intended beneficiary.

Some additional benefits that may be realized through an SNT are to provide (i) a level of asset protection against misuse of those funds; (ii) protection from claims from creditors, such as landlords, credit card companies, and other lenders, and (iii) proper investment management of the assets to increase the probability that they will meet the long‐term needs of the beneficiary. In creating an SNT, consider the benefits that a professional trustee may provide in terms of administering the trust.

Tax Planning Considerations

As more US taxpayers accumulate wealth for retirement inside of qualified retirement plans (such as 401(k), 403(b) and IRAs), there is growing deferred tax liability not only for the account owner, but also the legacy that they leave behind to others. Those qualified retirement assets are generally passed on to others in the form of an Inherited IRA.

An additional consideration for creating an SNT is that it may be designed to be the beneficiary of an Inherited IRA. The SNT will receive and administer the required minimum distributions (RMDs) received from the inherited IRA. While the default rule for most Inherited IRAs with an individual beneficiary is a 10-year distribution period, there is an exception to allow a disabled beneficiary to stretch the distributions out over their own life expectancy. However, if the trust is not drafted properly, not only could the distribution period for Inherited IRAs be reduced to just 60 months, but the trust might disqualify the beneficiary from receiving public benefits. Under previous law, to qualify for the extended life expectancy RMD term, a trust would be required to distribute IRA withdrawals to the beneficiary in the same year the trust received those withdrawals. These trusts are referred to as conduit trusts.

However, a change in the law at the end of 2022 now allows the trust to retain the IRA withdrawals inside the trust and still qualify to use the stretch method for calculating RMDs. The retention of IRA withdrawals in a properly structured SNT can enable the Inherited IRA assets to last longer due to increased tax deferral. Keeping funds in the SNT can also preserve the beneficiary's eligibility for government benefits.

There may be other considerations particular to a person's plan or circumstances. In the end, this is a process that should be done under the advisement of an attorney who specializes in planning for special needs. It is also helpful to engage a team of advisors who can help achieve the planning objectives through assistance with preparation of a long‐term cash flow analysis; design and implementation of the appropriate investment strategy; and ability to provide professional trustee services. In closing, an organized plan done with the right team can help ensure the needs of the beneficiary are met now and into the future.

Connect with a TD Wealth Advisor

Our TD Wealth Advisors are available for a consultation to start planning for your future.