You are now leaving our website and entering a third-party website over which we have no control.

Market Reflections: Investment Lessons Learned in 2025

(So Far)

By TD Wealth Chief Investment Office

As many students can relate to at this time of year, the end of a semester often marks an important period to step back and reflect on key lessons learned and, ultimately, how they can be applied. The same may be true for investors. In the opening months of this year the case studies have come fast and furious and we believe now may be an important point to take stock, tune out the headline noise, and consider some key investment lessons learned in 2025, so far.

Lesson #1: It pays to be persistent

On April 2nd the U.S. administration unveiled sweeping reciprocal tariffs which were higher and more far-reaching than many economists and investors had anticipated. The so-called 'Liberation Day' announcement imposed a double-digit levy on nearly all U.S. trading partners. Global equity markets and Treasury yields fell sharply on renewed uncertainty.

By the end of the first week of April, the S&P 500 Index of large-cap U.S. equites had recorded its largest two-day decline since March 2020, shifting lower by more than 10%. Investors had every reason to feel anxious about the direction of future returns and the prospect of meeting their financial goals. However, this was an event-driven correction and less than a week later a pause on most of the higher reciprocal tariffs helped to drive Index gains of almost 10% in a single day.

For all this excitement, the S&P 500 ended just slightly lower for the month of April. While this type of volatility may never be comfortable, it isn't unique. Historically, some of the very best days in financial markets have occurred during periods of significant volatility. Over the last 30 years, some of the strongest daily gains for the S&P 500 Index occurred in October of 2008 (during the Global Financial Crisis) and March 2020 (in the depths of the COVID-19 pandemic), months when the Index declined by approximately 11% and 12%, respectively.

The lesson here is straightforward – when it comes to uncertainty, markets may be quick to react, but investors don’t need to be. Making the mistake of selling when the market is falling can result in missing the subsequent bounce-back in market performance. In fact, missing just the 10 highest-returning days over the past 30 years would have resulted in a $100,000 portfolio, fully invested in the S&P 500, missing out on over $1 million worth of gains, compared to staying invested.

Periods of heightened market volatility and uncertainty are unlikely to end with the month of April but 2025 has already served as an important reminder that time in the market can be more important than timing the market. Investors, who have focused on their long-term plan, have historically achieved greater outcomes. It pays to be persistent.

Lesson #2: Nothing tastes better than a free lunch

Harry Markowitz, Nobel Prize-winning economist and father of modern portfolio theory, famously declared that when it comes to investing "the only free lunch is diversification". When it comes to building a portfolio, risk can be effectively reduced without sacrificing expected returns, simply by diversifying your investments.

Instead of trying to chase the latest winner, investors should instead focus on establishing a properly diversified portfolio. We believe a well-balanced portfolio, paired with a long-term, goals-based view, should help to soften the impact of a short-term spike in volatility, without letting emotions get in the way.

In 2024, for example, investor enthusiasm surrounding a small group of technology-focused companies helped to lift the Russell 1000 Growth Index by an impressive 33% for the calendar-year period. In contrast, a simple balanced portfolio with 60% invested in the broad S&P 500 and 40% in the Bloomberg Barclays US Aggregate Bond Index was ahead by a relatively modest 15%. For many investors, it was hard to get enough of a good thing.

In just the first four months of 2025, however, all that changed. By the end of April, growth-style U.S. equites were among the weakest performing of major asset classes, quickly declining by more than 8% while the balanced portfolio was more stable, down by less than 2% over the same period.

Sudden reversals in market leadership highlight the need for and benefits of creating balanced portfolios. Diversification provides exposure to a much wider opportunity set of investments and may help to mitigate losses during severe market downturns, leading to shorter recovery times.

While winners can keep winning for some time, leadership among asset class, sector, style, capitalization and geography – among other factors – will change and knowing which factor will lead is impossible to predict with any consistency. For long-term investors, variety may be more than just the spice of life. Take the free lunch.

Lesson #3: Personal finance is more personal than finance

Human emotions can play an important role in determining both investment decisions and outcomes. Even for more seasoned investors, longer-term financial goals and objectives may, at times, be at odds with their most basic emotional impulse. Faced with perceived threats to their financial security, investors may revert to a primal fight-or-flight response, resulting in irrational and short-term decision making.

Prospect Theory was first developed by psychologists Daniel Kahneman and Amos Tversky back in the 1970s and helps to make some sense of such a response. Their seminal work identified the concept of "loss aversion" as being part of our hardwired preference to avoid losses, even to the detriment of future gains. In fact, supporting academic studies suggested that the psychological pain of loss is twice as much as the pleasure received by equivalent gains.

The opening months of 2025 have shown this concept in action. How much easier is it for investors to recall the anxiety associated with steep market drawdowns in April, following the tariff announcements, than the events that led to earlier gains and a fresh all-time high for the S&P 500 Index in mid-February? Or even the subsequent recovery of all April losses by the same Index in early May?

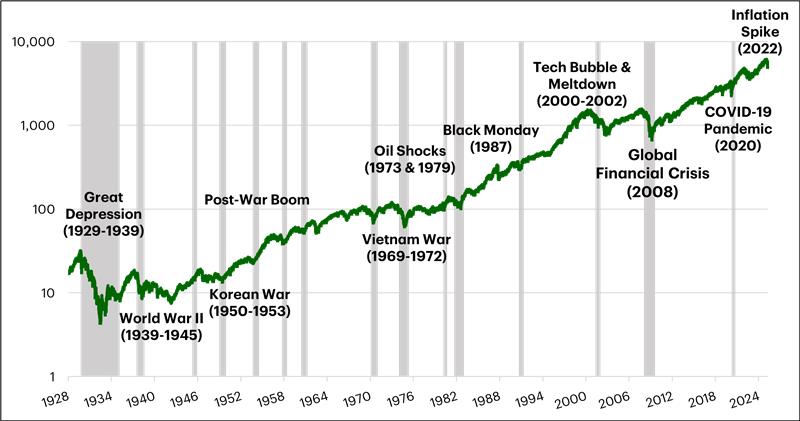

At the height of market corrections, individuals may be tempted to make investment decisions that put their long-term financial goals at risk. In such periods it is important to keep volatility in perspective. Over the last 50 years, for example, the S&P 500 Index of large cap U.S. companies has endured periods of economic stagflation, geopolitical tensions and wars, the bursting of a technology bubble, a global financial crisis and the COVID-19 pandemic. While the drivers and time periods may differ, history has shown that economies and financial markets are often more resilient than expected. Faced with losses, cashing out may appease our emotional bias but subsequent recoveries have rewarded patient investors (see Lesson #1).

Having a disciplined approach to the “personal” part of finance can be one of the most important aspects of successfully managing your finances, especially in today’s economy. When emotions are running high, sometimes the most valuable asset an investor can have in place is a thoughtful and well-defined financial plan.

Long-term S&P 500 Index returns have been strong despite periods of elevated volatility

S&P 500 Price Index, Log Scale

Source: FactSet, TD Wealth Chief Investment Office as of May 2, 2025. All performance is in U.S. dollars. Past performance is not indicative of future results. The indices are a tool to compare the performance of one or more indices. The volatility and performance of the indices may be greater than or less than the volatility and performance of actual investments. Indices reflect the reinvestment of dividends and income. Indices do not have fees, expenses or taxes, which would lower performance. Indices are unmanaged and not available for direct investment.