You are now leaving our website and entering a third-party website over which we have no control.

Understanding Fees

A lot goes into building and managing a mutual fund portfolio or exchange-traded fund (ETF). Understanding how much your investments cost is an important component when making informed investment decisions. It's equally important to know that cost alone doesn't always determine everything or provide the greatest value.

What is Total Cost Reporting (TCR)?

Total Cost Reporting (TCR), also known as Client Relationship Model Phase 3 ("CRM3"), is a new Canadian regulatory requirement designed to enhance transparency of investment fund costs. TCR represents the next phase of change following the launch of "CRM2" in 2016, which required dealers and advisors to deliver clients an annual performance report and an annual charges and compensation report. TCR introduces changes to the annual charges and compensation report by including the embedded costs of investment products in both dollar terms and percentage terms. Beginning in 2027, investor statements will disclose fees associated with qualifying investment types such as mutual funds and exchange-traded funds (ETFs).

With TCR there are no new fees — the goal is greater transparency.

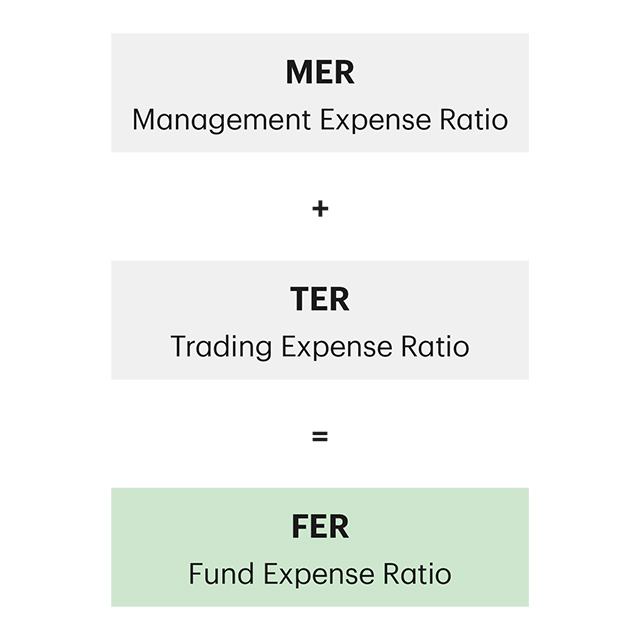

MER

Investment management

- Professional investment management, research, risk control, fund administration, support services

Operating costs

- Accounting, auditing, record-keeping

Taxes

- GST/HST

TER

Portfolio Transaction Costs

- For certain securities (e.g. equities)

FER

With Total Cost Reporting, clients will now see FER

Investment management

- Professional investment management,

research, risk control, fund administration,

support services

Operating costs

- Accounting, auditing, record-keeping

Taxes

- GST/HST

Portfolio Transaction Costs

- For certain securities (e.g. equities)

With Total Cost Reporting, clients will now see FER

MERs and TERs are calculated twice a year and included on regulatory documents like Fund/ETF Facts, and Management Reports of Fund Performance (MRFP). They are also posted on the TDAM website. As such, there may be situations due to timing or other factors such as fee changes where there is a discrepancy between what is displayed on these regulatory documents or TDAM website, and the FER that appears on a client statement.

-

Management Expense Ratio (MER)

-

Trading Expense Ratio (TER)

-

Value of Fees

Experience the value of professional investment management.

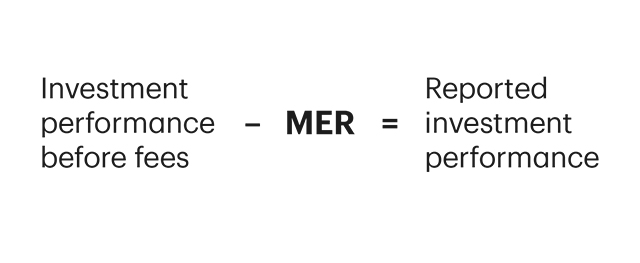

Mutual fund costs are typically expressed as a Management Expense Ratio, or MER. The fund costs that make up the MER are not charged to investors directly. Rather, the MER is reflected in the net return of a fund.

The MER is the cost of investing in a mutual fund or ETF. MER’s are calculated twice per year. A fund’s MER is its total management fees and operating expenses for the 6-month or 1-year period respectively expressed as an annualized percentage of its average assets over that time period. This includes the Fund’s proportionate share of the MER of any underlying fund, including ETFs, in which the Fund has invested. The MER includes GST and HST but excludes trading expenses.

MERs vary, depending on the type of fund, the series and how actively managed it is. For example, index funds generally have very low MERs. That’s because their objective is simply to match a market index. The more active, the more specialized (e.g. sector specific funds) or the more complex (e.g. Emerging markets funds), the higher the MER. Active investments aim to outperform the index, and require the specialized expertise of a professional fund manager backed by a team of dedicated researchers and analysts.

What are the components of an MER?

Fees | You can benefit from: |

| Management Fee Paid to the investment management firm |

|

Trailer Fee Paid to the investment management firm (not applicable to F-Series funds) |

|

Operating Costs Cover accounting, audit costs and record keeping |

|

Taxes GST and QST or HST | |

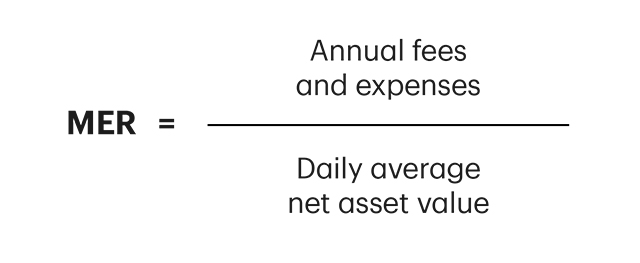

How is annual MER calculated?

A fund's MER is an annual fee representing the costs associated with investing in the fund throughout the year. The MER is expressed as a percentage of daily average net assets during the year:

How does the MER affect my return?

The MER is not paid by you directly, but it reduces your annual return. The MER is deducted before the investment performance is calculated and is reflected in the net return:

Does the MER include all costs?

The MER usually accounts for most of the fees you pay when investing in a fund, but it does not cover every expense:

- For equity funds, costs related to portfolio transactions — such as brokerage commissions — are excluded from the MER

- These trading expenses, paid by the fund manager, are reported separately as the Trading Expense Ratio (TER), which is considered a necessary part of fund operations

- You can find details about TERs in the Fund Facts document provided to all investors before making an investment. Select the "TER" tab above for more information.

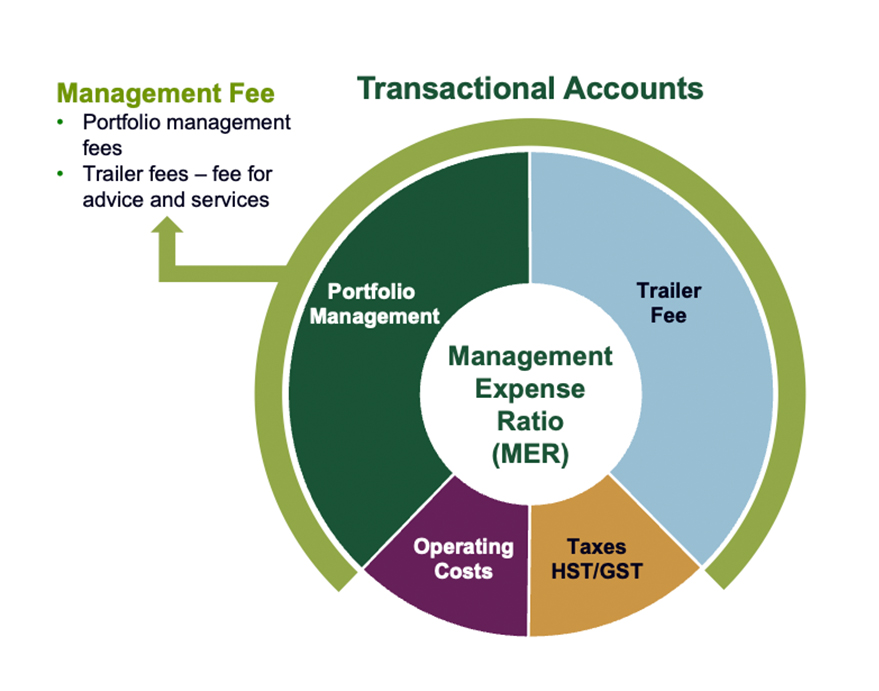

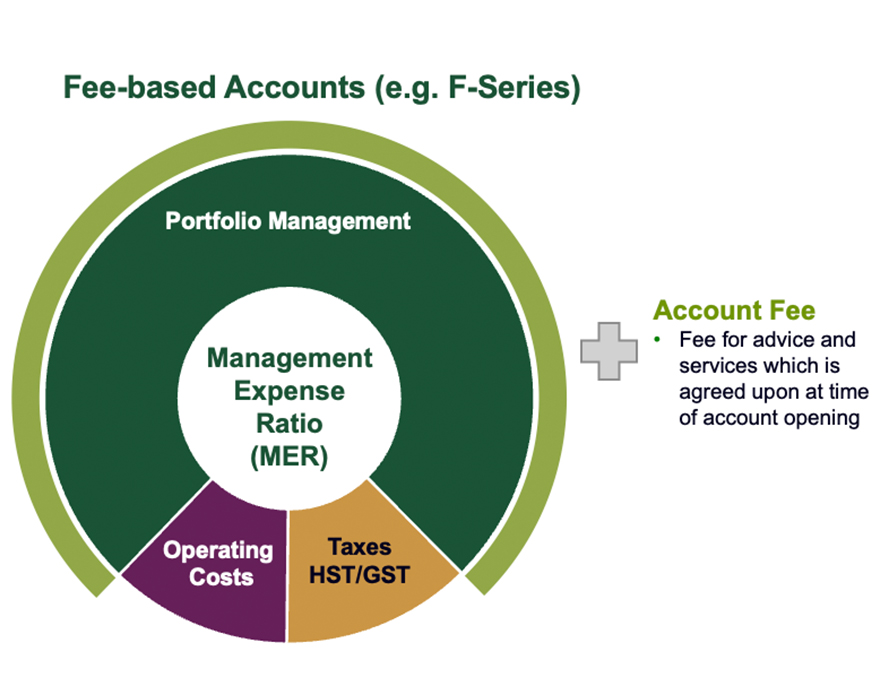

Are there differences in MER between transactional (e.g. A-Series) and fee-based (e.g. F-Series) accounts?

The components of an MER may differ across series of the same fund. For example:

Advisor Series (A-Series)

- These include a management fee (a combination of investment management expenses and, where applicable, trailing commissions), plus operating expenses and taxes

Fee-based Series (F-Series)

- These are offered through fee-based accounts, where the MER includes investment management fees, operating costs, and taxes

- Unlike other account types, fee-based accounts do not have trailing commissions. Rather, the firm that employs the advisor bills the investor directly for advice, access, and service.

TER Explained

The TER represents the cost of trading the portfolio management team incurs for buying and selling certain securities (e.g. equities) within a given fund. Trading expenses also occur for funds that trade derivative products—for example, certain funds (such as TD Alternatives Commodities Pool) have a TER but do not trade equities. Already published in regulatory documents like the Management Report of Fund Performance, the TER is also disclosed in the Fund Facts document which is required to be provided at point of sale.

Do all funds have a TER?

TERs most typically apply to funds that hold equities, however, funds that hold products like derivatives (e.g. options, futures) can also have expenses related to trading

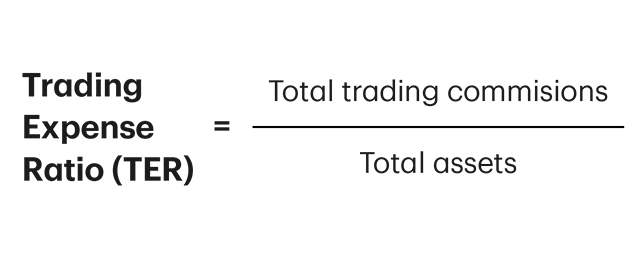

Most fixed income funds do not have a TER because commissions for fixed income funds are already embedded in the price of a bond. Fixed Income Funds that use derivatives for hedging or other purposes may have a TER association with those transactions. The TER is expressed as an annualized percentage of daily average net asset value during the period. This percentage is determined by dividing the fund’s total trading commissions incurred over a reporting period by the fund’s total assets.

How do TERs work?

The TER is shown as a yearly percentage based on the fund’s average daily net asset value ("NAV") for the period. This figure is calculated by dividing the total trading commissions the fund pays during the reporting period by its total assets.

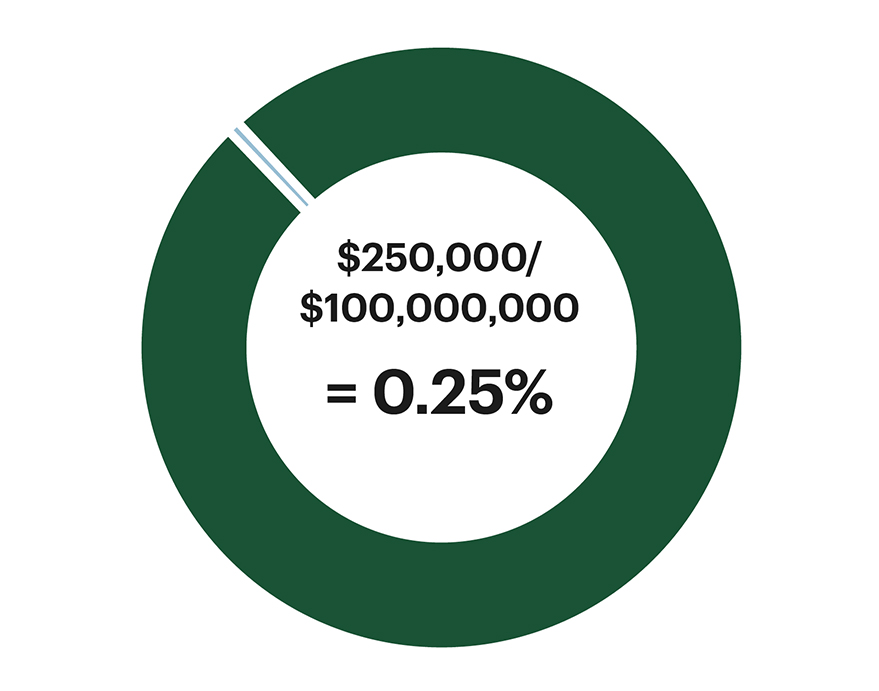

Example

Let's assume a fund manages $100 million in assets, and its portfolio managers generate $250,000 in trading commissions during a particular year. In this case, the fund’s TER would be calculated as show in this pie chart (for illustrative purposes only).

Combining the MER and TER components creates the Fund Expense Ratio (FER). With Total Cost Reporting (TCR), investors will see their personalized total amount paid to investment fund companies, in dollar terms and a breakdown of the embedded FER for any qualifying investment fund owned during the year.

Putting a price on expertise and advice.

A mutual fund or ETF’s MER makes it possible to have teams of investment professionals researching and managing the securities for the benefit of investors in the fund. An actively managed fund tends to have a higher MER since holdings are individually researched, selected and monitored. On the other hand, a passive fund, such as an index fund, tends to have a lower MER because holdings are passively selected from an index or benchmark.

A professionally managed TD Fund gains you access to our experienced portfolio managers, giving you the potential to:

- Outperform an index

- Build a more diversified portfolio than you likely could on your own

- Benefit from disciplined risk management

- Benefit from research, investment selection and professional money management

The MER may include a trailing commission for the services and advice provided by your advisor and their firm. The services and advice may include:

- Identifying investment solutions to help you reach your financial goals

- Helping to diversify your investments based on your risk tolerance

- Recommending changes to your investment portfolio as your financial situation changes

Professional portfolio management from TDAM:

- New Thinking: Innovative investment solutions that aim to bring new thinking to the most important challenges facing our clients and help them achieve their financial goals.

- Depth of Experience: Expertise across traditional and alternative solutions, with over 320 investment professionals working for you including a team of multi-disciplinary Portfolio Managers who have an average of 22 years’ experience. Our broad selection of strategies and solutions includes fundamental equities, quantitative and passive equities, fixed income across the credit quality spectrum and alternatives, such as private credit, infrastructure and real estate.

- Disciplined Risk Management: A disciplined and objective research process with a focus on in-depth analysis of company and industry fundamentals

- Trust: We have been in business for more than 35 years, and over that time the investment landscape, investor needs, and our range of offerings have evolved. What has remained consistent is our focus on quality, our risk management discipline and our commitment to our clients.

The information contained herein has been provided by TD Asset Management Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

Commissions, management fees and expenses all may be associated with mutual fund and/or exchange-traded fund ("ETF") investments (collectively, "the Funds"). Trailing commissions may be associated with mutual fund investments. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns. Please read the fund facts or ETF Facts and the prospectus, which contain detailed investment information, before investing in the Funds. The Funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated.

TD Mutual Funds are managed by TD Asset Management Inc., a wholly owned subsidiary of The Toronto-Dominion Bank, and are available through authorized dealers. TD ETFs are managed by TD Asset Management Inc., a wholly-owned subsidiary of The Toronto-Dominion Bank.