You are now leaving our website and entering a third-party website over which we have no control.

Published: December 3, 2025

Investor Knowledge 10 minutes

The Science of Stability:

Building Resilient Portfolios with Core Bonds

Share

![]()

![]()

![]()

![]()

David Tallman, CFA

Vice President and Director, Client Portfolio Mgmt.,

TD Asset Management Inc.

Sayada Nabi

Associate, Fixed Income, Client Portfolio Mgmt.,

TD Asset Management Inc.

Think of fixed income as the ballast in a ship. A ship without ballast may sail quickly in calm waters, but the moment the waves get choppy, it risks capsizing. Similarly, a portfolio without fixed income may soar in bull markets but can easily sink in volatile times. Fixed income is often best thought of as "portfolio insurance", but uniquely, it’s insurance that pays you an income while you wait.

So, let’s explore why core fixed income deserves a starring role in your long-term investment plan.

Bond Basics

Investors were initially drawn to bonds because they knew what prolonged stock market downturns felt like and how bonds could help. Forgoing upside for certainty, bonds aim to provide investors predictable income and capital preservation through contractual interest and principal payments. Core fixed income refers to the high-quality, broadly diversified portion of the bond market, with the key tenets being steady income and portfolio diversification. These pillars tend to become especially important when riskier parts of a portfolio come under stress, reinforcing the foundational value core bonds bring to a portfolio's fixed income allocation.

Key pillars of fixed income

|

Understanding the Four Factors that Impact Fixed Income Returns

From far away, fixed income investments appear the same in that they are loans that trade predictable income for less of an upside/growth. Under closer inspection, however, they are not all built the same

and have material differences. Understanding the key levers that impact the risk/return drivers for each unique bond can help investors build a more resilient portfolio and put them closer to their long-term financial goals.

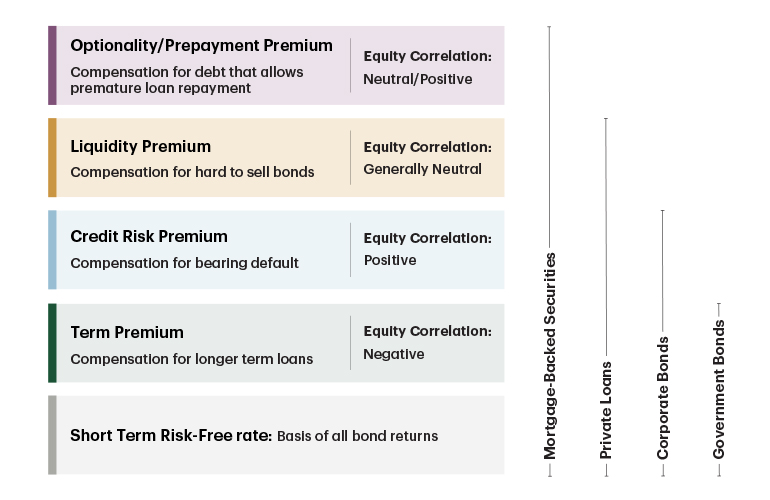

There are four key building blocks that help shape return expectations for any given bond, but each bond is exposed to these elements at varying degrees (Figure 1). Each building block carries its own risk, reward, and relationship to the broader equity markets:

Term (duration) Premium – The sensitivity of a bond’s price to changes in interest rates. When interest rates fall, bond prices rise. In an economic slowdown, where stocks lose value and interest rates decline, bond prices tend to move up. The inverse relationship duration has with equities tend to make bonds a natural hedge during episodes of market volatility. This is the prevailing factor that influences government bond returns.

Credit Premium – The reward investors receive for taking on the risk that a borrower won’t pay back what they owe. Government Treasuries in highly developed countries, like the U.S, have virtually no credit risk, whereas Investment-Grade Corporate Bonds can carry some, and High-Yield Bonds may carry more. Credit risk tends to move in the same direction as equities. When corporate earnings are under pressure, both stocks and bonds with material credit risk tend to suffer.

Liquidity Premium – Additive yield to compensate for hard to sell bonds. Private loans or less liquid bonds usually offer investors higher yields to account for this inconvenience. It largely has a neutral relationship with equities. In stable times, it may not correlate strongly with equities, though in stressed markets, liquidity could dry up.

Optionality / Prepayment Premium – Receiving principal loan payment prematurely, which then leads to loss of future interest income. This is common in some securities, like U.S. mortgage-backed securities (MBS) which can give borrowers the option to pay back early if interest rates drop. While that’s a benefit for the borrower, it’s a drawback for the lender because it shortens the bond’s life and may reduce the income stream you were counting on. Prepayments pick up when rates fall or when housing/credit conditions strengthen. As such it is generally neutral or slightly positively correlated with equities.

Figure 1: Each type of bond is exposed to return drivers at varying degrees

Source: TDAM

For illustrative purposes only. Risk premiums will vary per bond and security type. Exposure to various risk premiums affects a bond’s price, income, and its overall value. The short-term risk-free rate is a reference point for all financial assets, representative of expected return on investment that carries no risk.

This interplay is what makes fixed income more than just “boring bonds”—each risk/return driver can behave differently depending on the market environment, while duration (term premium) stands out as it tends to be the clearest equity diversifier. Different fixed income strategies harness different combinations of these drivers.

Given that core bonds have a meaningful allocation to the duration risk/return driver through government bond holdings, and additional income through high-quality corporate bonds, they generally satisfy the key role of fixed income (effectively its portfolio insurance that pays you an income). If investors want to increase their income by utilizing different return drivers, they can maintain their "portfolio insurance" by complementing their core bond holdings with some of the above strategies mentioned or by investing in a core "plus" strategy with additional income levers.

Don’t Overlook the Quiet Hero

It’s not just about math, it’s about psychology. Investing is as much about behaviour as it is about numbers. When stocks fall sharply, many investors panic and sell at the wrong time. Bonds can help provide the emotional ballast that helps people stay invested. Knowing a portion of your portfolio is stable makes it easier to weather storms without abandoning your long-term plan.

Core fixed income may not generate the excitement of the latest tech stock or cryptocurrency. But its role in a portfolio is critical — like the foundation of a house, the keel of a boat, or the seatbelt in your car. It can help protect, stabilize, and support growth by giving investors greater confidence to stay the course.

As you think about your financial goals — whether building wealth, funding retirement, or simply sleeping well at night — remember that stocks may be the engine, while bonds often serve as the steering wheel and brakes. You need all three to reach your destination safely.

The information contained herein has been provided by TD Asset Management Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.