You are now leaving our website and entering a third-party website over which we have no control.

TD Wealth Market Insights: July 2025 Snapshot

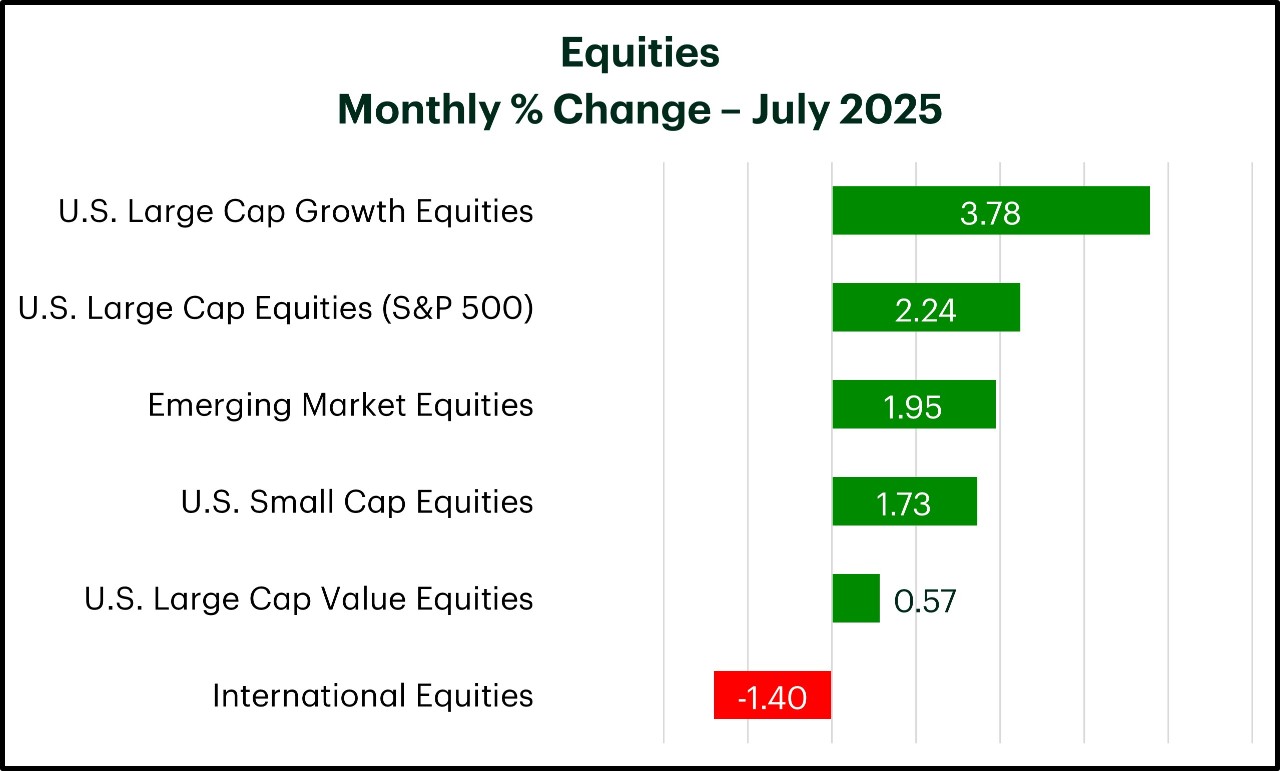

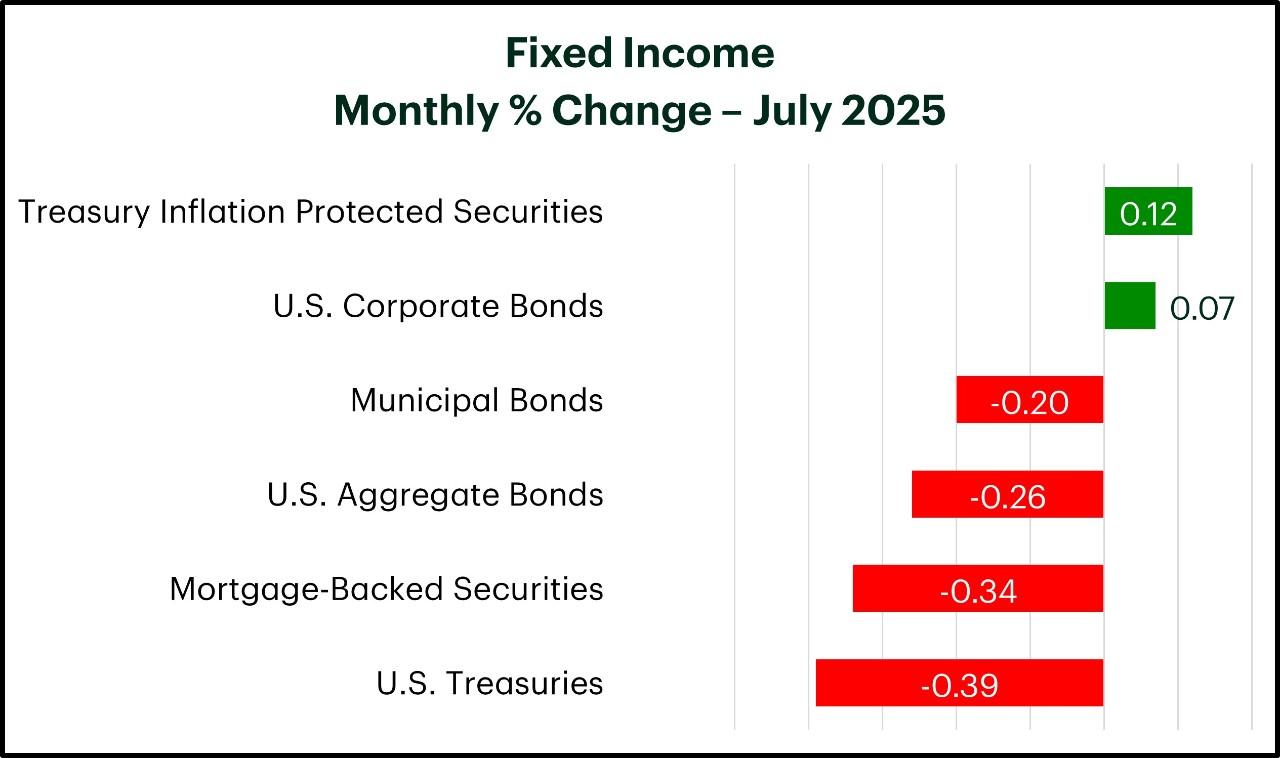

Source: Morningstar, TD Wealth Chief Investment Office. Indices used include the Bloomberg US Treasury TR Index, Bloomberg US Aggregate Bond TR Index, Bloomberg US Corp Bond TR Index, Bloomberg US Treasury US TIPS TR Index, Bloomberg Municipal TR Index, Bloomberg US MBS Float Adjusted TR, ICE BofA US High Yield Constrained TR Index, S&P 500 TR Index, Russell 1000 TR Index, Russell 1000 Growth TR Index, Russell 1000 Value TR Index, Russell 2000 TR Index, MSCI EAFE NR Index, and the MSCI EM NR Index, LMBA Gold Price PM, WTexas Crude Int Oil BL. All performance is in U.S. dollars. Past performance is not indicative of future results. The indices are a tool to compare the performance of one or more indices. The volatility and performance of the indices may be greater than or less than the volatility and performance of actual investments. Indices reflect the reinvestment of dividends and income. Indices do not have fees, expenses or taxes, which would lower performance. Indices are unmanaged and not available for direct investment.

Monthly Market Brief Commentary – July 2025

-

1

Market Momentum: Equities continued to advance in July with the S&P 500 Index of U.S. companies notching its third consecutive monthly gain and setting a fresh all-time high along the way. Technology emerged as a key driver of performance as earnings growth and the prospect of advances in Artificial Intelligence helped to fuel investor optimism. While major domestic stock markets were positive, international developed equities gave back some of their strong year-to-date gains in U.S.-dollar terms, as the value of the dollar rebounded. Despite lofty market valuations and pockets of near-term uncertainty, we believe maintaining a diversified portfolio with exposure to a wide range of asset classes, sectors and geographical regions can provide investors with the opportunity to benefit from multiple drivers of return over time.

-

2

Fiscal Focus: The One Big Beautiful Bill Act was passed into law early in July. While congress remained divided on elements of the budget bill, its passing ensured an extension of the Tax Cuts and Jobs Act and helped to provide greater clarity on fiscal spending priorities with a renewed focus on deregulation and growth. In the aggregate, the budget bill is set to significantly augment fiscal deficits over the next 10 years, with estimates running in the $3-$4 trillion range. The bill front-loads the costs and back-loads the savings, which should result in an early boost to economic activity. While the projected growth for this year remains largely unchanged, we expect a modest boost to GDP growth for 2026.

-

3

Progress to Trade: July marked the end of a 90-day tariff pause with the deadline for trade negotiations further extended to August 1st. U.S. trade policy however remained in flux with countries and industries regularly targeted by new and higher tariff rates. Importantly, progress was made in reaching trade agreements with key U.S. trading partners, including Japan and the European Union (E.U.). In aggregate, the E.U., along with China, Mexico and Canada, represent over three-quarters of all U.S. exports and imports. Long-term trade agreements with these regions remains central to the path of inflation and outlook for economic growth.

TD Wealth Asset Allocation Views – August 2025

INVESTMENTS, SECURITIES AND ANNUITIES |

||||

NOT A DEPOSIT |

NOT FDIC-INSURED |

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY |

NOT GUARANTEED BY THE BANK |

MAY GO DOWN IN VALUE |

TD Economics Key Financial Forecasts