You are now leaving our website and entering a third-party website over which we have no control.

Fall 2025

James H. Beam Jr.

Head of TD Wealth Planning, Retirement & Strategy (U.S.)

Mark D. Hasenauer

TD Wealth – Planning & Goals Based Advice Leader

Ashley W. Weeks

Editor-in-Chief TD Wealth – Wealth Strategist

Featured Articles

INVESTMENTS, SECURITIES AND ANNUITIES |

||||

NOT A DEPOSIT |

NOT FDIC-INSURED |

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY |

NOT GUARANTEED BY THE BANK |

MAY GO DOWN IN VALUE |

Perhaps the most impactful feature of the One Big Beautiful Bill is not what it changes, but what it makes permanent.

After months of posturing, fiery negotiations, and political horse trading, we now have signed legislation that outlines tax rules for the foreseeable future. While the One Big Beautiful Bill Act ("OBBBA") is a massive law with far reaching implications, the immediate concern for many retirees and near retirees is how it will impact their bottom-line during tax season.

The greatest attribute of the OBBBA is the certainty it provides for financial planning. Since the Tax Cuts and Jobs Act of 2017, we have contended with the looming threat of higher income tax rates and the sunset of several individual tax breaks in 2026. Now with the passage of the OBBBA, lower marginal individual tax rates are permanent, as are the higher standard deductions that were implemented in 2017. The new law also includes an assortment of novel tax breaks that can benefit retirees, though mileage may vary as specific rules and income phaseouts apply.

The following outline covers some key individual tax provisions of the One Big Beautiful Bill Act.

Permanent Updates Impacting Retirees (from the One Big Beautiful Bill Act)

The following provisions are now permanent fixtures in the federal tax code under the OBBA:

❖ LOWER INCOME TAX RATES

Prior to the OBBBA, five of the seven individual brackets would have seen higher marginal rates in 2026 with the top rate increasing to 39.6%. The lower marginal individual income tax rates that were first introduced for 2018 have now been made permanent.

❖ INCREASED STANDARD DEDUCTION

Around 90% of taxpayers now take the standard deduction since it was nearly doubled starting in 2018. The OBBBA makes the heightened standard deduction permanent with a slight increase. The 2025 standard deduction is $15,750 for single filers ($31,500 for joint filers). At age 65 single filers can add $2,000 to their standard deduction and joint filers can add $1,600 (per spouse who is age 65 and over).

❖ INCREASED ESTATE AND GIFT EXEMPTION

The heightened federal estate and gift exemption that was scheduled to sunset in 2026 has now been made permanent. The 2026 federal estate and gift exemption will be $15 million per person, and this figure will be indexed for inflation in subsequent years.

❖ CHARITABLE DEDUCTION FOR NON-ITEMIZERS

Starting in 2026, those who use the standard deduction ("non-itemizers") will be able to take a modest "above-the-line" deduction for cash gifts to charity. The limits for this deduction are $1,000 for single filers and $2,000 for joint filers.

Temporary Updates Impacting Retirees (from the One Big Beautiful Bill Act)

❖ ADDITIONAL "SENIOR DEDUCTION"

For tax years 2025 to 2028, taxpayers aged 65 and above will be able to take an additional $6,000 tax deduction, subject to income limits. This "senior deduction" is available for both itemizers as well as those who take the standard deduction (in which case this additional deduction would be added to the age 65+ standard deduction). Married joint filers who are both age 65 will received a combined $12,000 "senior deduction."

Income Limit: The "senior deduction" will phase out for higher income individuals based on modified adjusted gross income:

Single Filers – The senior deduction phase out starts after $75,000 of modified adjusted gross income (MAGI) and is fully phased out at $175,000 of MAGI.

Married Filing Joint – The senior deduction phase out starts after $150,000 of MAGI and is fully phased out at $250,000 of MAGI

❖ INCREASED STATE AND LOCAL TAX DEDUCTION

For tax years 2025 to 2029 the itemized deduction for state and local taxes ("SALT") has been increased from $10,000 to $40,000, subject to income limits. In 2030 the prior $10,000 cap will be reinstated.

Income Limit: Once modified adjust gross income (MAGI) exceeds $500,000 (for single & joint filers) the increased SALT deduction will be reduced by 30% of the excess MAGI over $500,000 in 2025. These figures will be indexed for future years and the deduction will not be reduced below $10,000 regardless of income

Odds and Ends and Final Thoughts (from the One Big Beautiful Bill Act)

In addition to provisions that are likely to have a broad impact on retirees, the OBBBA includes a patchwork of novel tax breaks with varying utility depending on individual circumstances. A few of the highly publicized temporary new deductions that are available regardless of whether an individual itemizes include:

Tax Break for Tips

- Tax years 2025 to 2028 only.

- Workers may be able to deduct up to $25,000 of tip income.

- Income phase out starting at $150,000 MAGI for single filers and $300,000 for joint filers.

Tax Break for Overtime

- Tax years 2025 to 2028 only.

- Workers may be able to deduct up to $12,500 ($25,000 for joint filers) of "qualified overtime compensation."

- Income phase out starting at $150,000 MAGI for single filers and $300,000 for joint filers.

Tax Deduction for New Car Loan Interest

- Tax years 2025 to 2028 only.

- Purchasers of new personal use vehicles assembled in the US may be able to deduct up to $10,000 of auto loan interest.

- Income phase out starting at $100,000 MAGI for single filers and $200,000 for joint filers.

While this summary only scratches the surface, it is important to reiterate the greatest attribute of this legislation is the certainty we now have around tax policy going forward. Perhaps the most impactful feature of the One Big Beautiful Bill is not what it changes, but what it makes permanent, specifically lower tax rates and a larger standard deduction that will literally take an act of congress to reverse in the future.

Investors and retirees should take this opportunity to reengage their financial plan with a fresh sense of clarity regarding the tax landscape.

TD Bank conducted its first-ever Financial Preparedness Report, Consumer Index, surveying more than 5,000 U.S. adults in 2025.

The survey examined respondent's financial challenges, savings habits, and the actions they are taking to improve their financial health. The survey's goal was to learn more about consumer's financial preparedness, while sharing these results to help them understand positive actions they can then take going forward.

The survey uncovered some staggering statistics, including that more than one-third of respondents do not feel they have enough savings to cover unexpected bills, while almost one-half added they do not feel prepared for retirement either.

On the positive side, most respondents are taking steps to improve their financial situation and maintaining both physical and mental health are broadly seen as key priorities.

Several important survey findings that impact retirement planning are outlined on the following charts. Full survey results can be accessed online at: stories.td.com/volumes/default/TD-Bank-Financial-Preparedness-Survey-2025Report.pdf

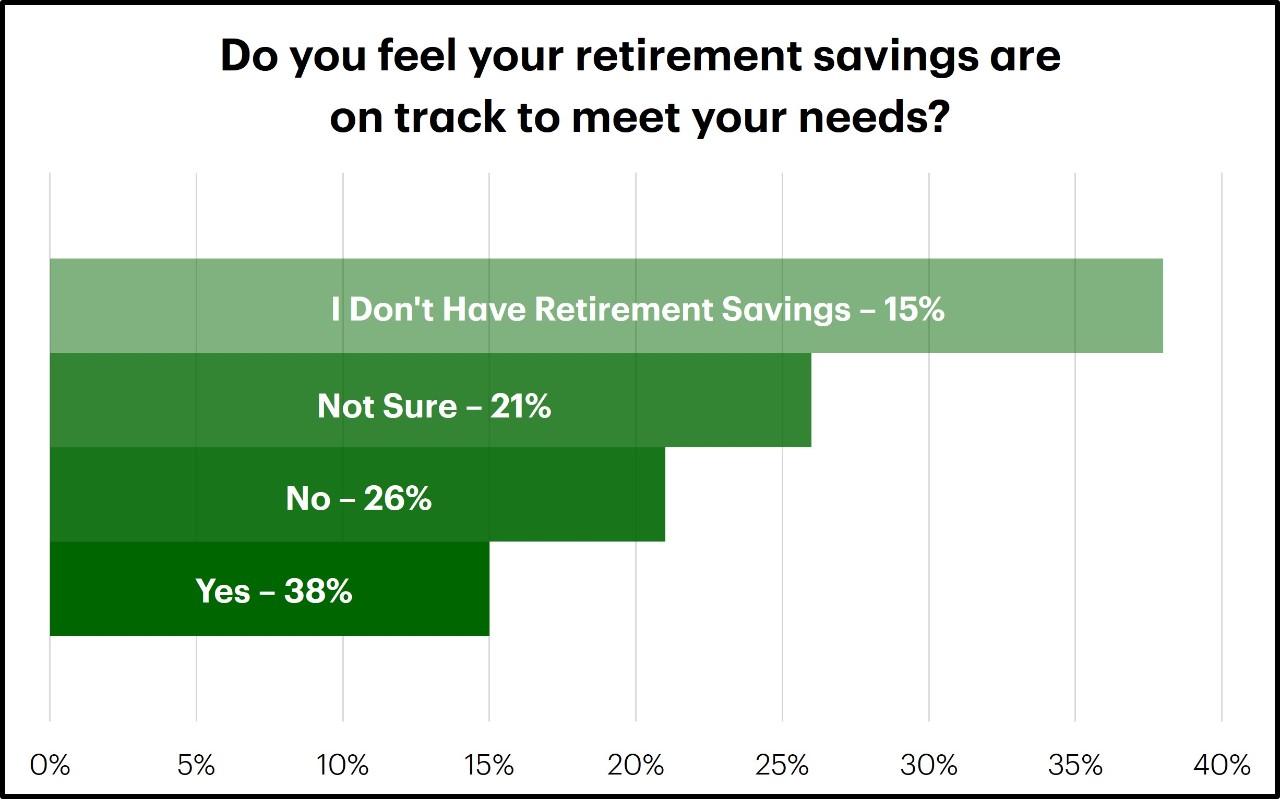

Survey Results: Retirement Savings on Track to Meet Needs

Just 38% of respondents say their retirement savings are on track to meet their needs, and 15% of respondents indicated they have no retirement savings at all.

Generational Divide:

The underlying data from the sample also indicates a sizeable generational variance in perceived retirement readiness. Baby Boomers reported the highest level of retirement readiness at 44% and Millennials were not far behind with 41% reporting they were on track. As a group, Gen X appeared the least optimistic with only 29% indicating they were on track for retirement and Gen Z fared only slightly better at 34%.

Survey Results: Monthly Income Set Aside for Retirement

About seven in ten respondents (69%) set aside money for retirement, including an employer match program. Nearly half contribute 10% or less of their monthly income, while 21% save more than 10%.

Observation:

Most experts suggest a retirement savings rate of at least 15% of income and the data gleaned from this survey corroborates recent studies that indicate consumers are falling behind with retirement savings.

Survey Results: Emergency Savings

Emergency savings are an often-overlooked part of retirement planning. Unexpected expenses can snowball into debt or early retirement account withdrawals. Most respondents acknowledge that they should have at least four months of living expenses in an emergency account.

However, when it comes to actual savings levels, just over one-third (36%) of respondents have at least four months of living expenses saved in an emergency fund.

Interested in more? For a recent TD MoneyTalk® video discussing some additional survey findings, please visit the following: Link to MoneyTalk Video

Transferring brokerage assets after the death of a loved one may feel like a bureaucratic ordeal for beneficiaries and executors. A basic understanding of the process can prevent frustration.

As soon as an investment firm learns of an account holder's death, all activity within that account is typically suspended. This means all trading and distributions will be frozen and open orders that have not been executed will be cancelled. To the all too frequent exasperation of loved ones, this also means that caregivers who previously assisted the account owner, and individuals authorized under a financial power of attorney, can no longer transact or manage the account.

Loved ones often seek immediate account access to cover a decedent's final expenses or to unwind volatile investment positions. However, investment firms are beholden to strict regulations designed to protect the decedent's estate and prevent unauthorized activity. The exercise of transitioning a decedent's brokerage account is document centric and knowing which forms to acquire can expedite the process.

The Paper Chase – Important Documents

Some (or all) of the documents outlined below will be necessary prior to transferring a decedent's investment accounts:

❖Death Certificate

In virtually every scenario where an account owner has died, the investment firm will require a death certificate. When beneficial parties like a designated beneficiary or a co-owner are predeceased, those death certificates will also be needed.

❖Legal Appointment

Investment firms will need to verify legal authority prior to taking directions regarding a decedent's account. If the brokerage account will pass under the decedent's probate estate, a recent court document appointing the executor will be required. In cases of trust ownership, an updated trust certification with clear trustee succession will be required.

❖Beneficiary Verification

In cases where a decedent's account passes directly to a beneficiary outside of probate, the investment firm is required to verify the identity of the beneficiary prior to taking instructions from them. This commonly occurs with transfer on death accounts (TOD/POD), as well as retirement accounts that have designated beneficiaries.

It is important to note that in instances where there is no surviving designated beneficiary of a retirement account, the default plan rules will apply and the investment firm will need to ascertain the identity of the default taker prior to transferring the account.

Establishing a New Account

It is typically prohibited for an investment firm to knowingly permit transactions to occur in an account that is titled to a deceased individual. Accordingly, once documentation establishing legal authority has been provided, a new account will be opened to receive the assets. This could be an estate account under the authority of the executor, an inherited IRA registered to the designated beneficiary, or even an individual account registered to a transfer on death (TOD) beneficiary. Only once the new account is established can assets be transferred over and managed by the legal representative or beneficiary.

Updating a decedent's brokerage account may seem like a headache, but understanding the sequence and key documents will simplify the process.

MEDICARE PREMIUMS

Don't let IRMAA catch you off guard!

There is a veiled trap for Medicare participants that can drastically increase costs. Premiums paid for Medicare Parts B & D are subject to something called the Income Related Monthly Adjustment Amount or "IRMAA" which increases premiums for higher income individuals. This increase can be substantial.

For 2025, participants subject to the largest IRMAA adjustment pay an additional $529.70 per month in Medicare premiums!

How is IRMAA calculated?

- Medicare looks at your tax return from two years prior, meaning 2023 tax returns were used to determine IRMAA increases for 2025.

- If your Modified Adjusted Gross Income "MAGI" (adjusted gross income plus tax exempt interest) exceeds certain thresholds, an increased premium will apply.

- Joint filers whose MAGI exceeded $212,000 ($106,000 for single) based on their 2023 tax returns have increased premiums for 2025.

- There are five brackets of increasing IRMAA adjustments depending on MAGI.

What can I do to plan around IRMAA?

As we approach the end of the year, now is a good time to take stock of your current tax position and understand that the tax return you file for 2025 will be used to determine Medicare premiums in 2027.

If your projected 2025 MAGI (Modified Adjusted Gross Income) is on track to exceed the IRMMA threshold, there are several strategies to consider:

- Use cash or Roth withdrawals for spending needs in lieu of realizing additional gains or withdrawing retirement funds that will be included in taxable income.

- Consider limiting taxable portfolio gains through tax loss harvesting.

- If eligible, contribute to a tax-deductible retirement account.

- Consider a Qualified Charitable Distribution (QCD) for IRA Required Minimum Distributions (RMDs) to avoid including the RMD as taxable income.

There are also a few caveats to take note of:

- Increasing itemized deductions will not reduce modified adjusted gross income as this figure is calculated before considering itemized deductions.

- Tax exempt interest from municipal bonds is added back to calculate modified adjusted gross income and does not help reduce IRMAA.

In some instances, you can request an IRMAA waiver for certain life changing events such as a change in marital status or job loss (among others). However, a one-time income event like selling real estate will not justify an IRMAA waiver.

Retirees who downsize and have a large taxable gain on the sale are sometimes startled when Medicare premiums skyrocket two years later. The silver lining for one-off income events is that the increased premiums only last for one year.

For additional information regarding 2025 Medicare costs and a complete breakdown of the Parts B & D income related monthly adjustment amounts, please visit: 2025 Medicare costs

Connect with a TD Wealth Advisor

Our TD Wealth Advisors are available for a consultation to start planning for your future.