X

How to use your new student credit card

Now that you’re in university/college/trade school, you’re going to receive plenty of opportunities to apply for a credit card. But do you know the fundamentals? We’ll give you some key info, so you can be more confident about using a credit card after you’ve been approved for one.

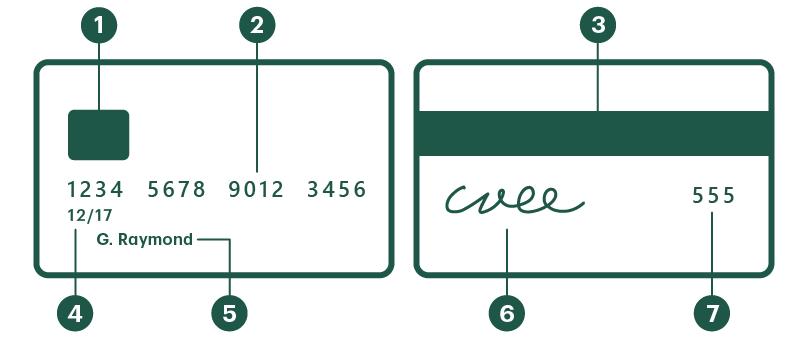

Anatomy of a credit card

Here are all the bits and pieces of your credit card.

1. Security chip

2. Account number

3. Magnetic strip

4. Expiration date

5. Cardholder's name

6. Signature

7. Security code (CVV/CVC)

Let’s start from the beginning

When you apply for a credit card, you’re essentially borrowing money from the bank. So when you buy something on your Credit Card, say $210 worth of textbooks from the bookstore, the bank pays this amount on your behalf. Then, at the end of your monthly billing cycle, you’ll receive a bill (called your monthly Credit Card statement), with the amount you must pay back to the bank.

Lucky for you, you get something called an “interest-free grace period” for any purchases you make with your card.

It’s the period of time when the purchases you make do not accrue any interest provided you pay your balance in full by the payment due date shown on the monthly statement.

But what if you can’t pay the balance in full?

If you can’t pay the balance in full by the payment due date-don’t freak out. There is a smaller amount you can pay called the Minimum Payment Amount. Now this amount you need to pay by the payment due date. Paying your Minimum Payment Amount on time will ensure that you keep a good credit rating.

Keep in mind that paying only the minimum amount is very costly because the interest on those remaining charges will continue to grow.

A word of warning-if you don’t make the Minimum Payment Amount or if you don’t pay it by the payment due date, your credit score starts to go down. The interest rate that applies to your purchases and cash advances may also be increased. And if you miss too many payments, you could ultimately lose your Credit Card. Nobody wants that. So use your Credit Card responsibly.

And if you make a habit of only paying the Minimum Payment on the payment due date, it could take you years to get out of debt.

Long story short-use your Credit Card wisely

At the very least, every month you should be paying your Minimum Payment Amount by the payment due date. But try not to make a habit of only paying the Minimum Amount. Your monthly statement will tell you how long it will take to pay off your entire balance if you only pay the Minimum Payment Amount each month. The length of time could shock you (think decades, not years). So if you can pay more than the Minimum Payment Amount, or even the full amount, then do it.

Share this article