Canada

Canada

US

US

Tips for setting your financial priorities

Excerpts of a TD Newsroom article on the same topic published September 7, 2020

Before you can explore how to create a financial plan, review and set your financial priorities, as well as develop a sound savings habit.

Cyrus Pourmoslemi, TD advisor suggests the following four tips to his clients who are looking to review their financial priorities in the face of a crisis, and these tips may help you too:

1. Understanding your cashflow

Understanding your cashflow is always important, especially after an unexpected financial event. In any case, knowing how much money is coming in and how much is going out is key.

"As a first step I'd recommend breaking your pay cheque or whatever cashflow is coming into your household to see how much of it must go to cover your necessary needs and expenditures and then determine if any monies remain to apply towards your wants or long-term savings," he said.

"Using a personal cashflow calculator can really help with this exercise, instead of spending hours putting together an updated budget with several categories for expenditures."

2. Pay attention to changes in your financial situation

Pourmoslemi says choosing between saving any extra funds available (once you've addressed your basic needs) or using them to pay off debt is a question many Canadians struggle with, and what to do depends on a variety of factors, including:

- The interest rate environment

- Your short and long-term goals

- Your debt load, including mortgages

- Your current overall financial picture

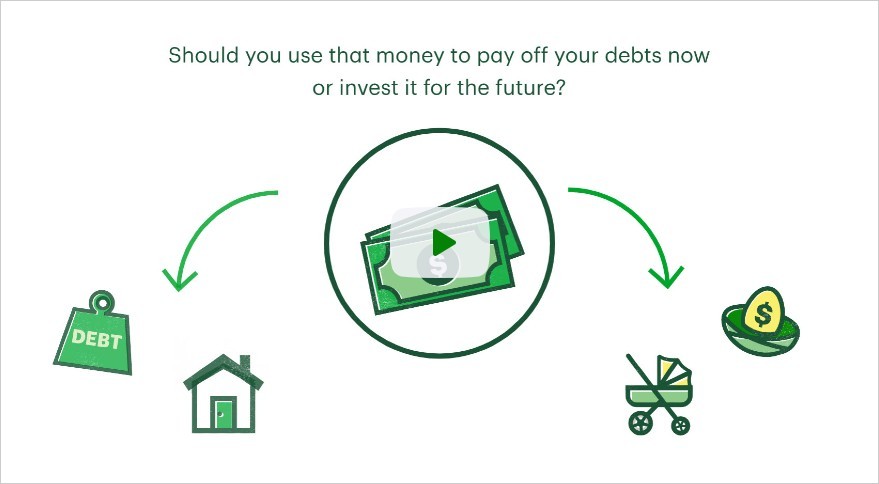

Deciding how to allocate your hard-earned pay is not always easy. Especially if you come into some extra cash and have to decide between paying down debts or investing for the future. Comparing the rate of return on your debt versus the return on any potential investments in this interactive video can help. It's just one aspect of setting your overall financial priorities.

3. Prioritize saving for a rainy day

It is often the case that building an emergency fund, no matter how small, with any money left once necessities are paid, can help to reduce financial anxiety for the future Pourmoslemi said. Setting aside some money on a regular basis, once necessities have been covered, to create an emergency savings fund, can also limit having to rely on using credit for an unexpected future expense.

If you find yourself struggling to save for a rainy day, Pourmoslemi said it's probably worth considering restructuring your debt which could help improve cash flow, but you should speak to an advisor to discuss your unique situation.

4. Don’t be afraid to seek help from a TD advisor

An advisor can help you to set your goals for the future using TD Goal Builder. They can also provide advice suited to helping you meet your goals based on your financial situation. Once your goals are set using TD Goal Builder, you will be able to keep track of your progress.

Many people are still intimidated when it comes to speaking to an advisor and talking about money, but a lot of good financial habits and strategies can come from breaking the ice and having that conversation.

Do not to be afraid to talk to an advisor, and when you do, ask questions to ensure you understand the advice being given.

5. Establish a savings habit with a pre-authorized transfer service

Even when cashflow is limited, establishing an emergency savings account can be done. To help slowly build up an emergency savings account, Pourmoslemi recommends considering using a pre-authorized transfer service (PTS).

This lets you set an amount of money that's automatically deducted from your account on a regular basis and deposited into a separate account so that you aren't tempted to spend it.

You can set one up online, choosing to deduct any amount on a schedule that works for you.

6. Start saving with small amounts

If a pre-authorized transfer service doesn’t seem like a possible strategy for you right now, setting aside small amounts each time you use your debit card is another savings strategy you could try.

TD customers who have a savings account can use our Simply Save program to top funnel money into your savings account. The program rounds up your debit card purchases by a minimum of fifty cents to a maximum of five dollars, as set by you, and places the extra rounded-up funds into your designated savings account. Pourmoslemi says this method of saving, while modest, can be a good way to start an important habit.

"Any amount is a good start when it comes to saving," he said.

"When you start seeing your savings balance grow, it can help motivate you to want to save more, including finding ways to reduce your spending as well. Doing this can help you focus on working towards achieving any long-term financial goals you may have in your financial plan."

This content discusses current topics of interest in a general and informational manner only and may not be appropriate in all circumstances. Please ensure that you seek advice personalized for your situation from the appropriate professional, consultant or subject matter expert on the topic of interest to you.

Share this article

Related articles

View personal banking updates and how we're ready for you.