You are now leaving our website and entering a third-party website over which we have no control.

IBOR Transition - Moving Away from LIBOR and CDOR

For decades, Interbank Offered Rates (IBORs) have been used as reference rates for trillions of dollars of financial products including derivatives, bonds, loans, securitizations, and deposit accounts at TD and other financial institutions in North America and around the world. However, a global interest rate benchmark reform effort has been in progress to transition from IBORs to alternative reference rates (ARRs).

This shift impacts several IBORs such as the London Interbank Offered Rate (LIBOR) – the most frequently used IBOR – and the Canadian Dollar Offered Rate (CDOR).

What clients can expect

The discontinuance of LIBOR and CDOR may affect your products and services. TD is actively engaging with industry bodies and market participants to support a smooth transition away from LIBOR and CDOR. TD has and will make every effort to inform you of any significant market developments.

TD recommends that you review your IBOR exposures, as well as contracts with an IBOR reference, and work with your independent financial and legal advisors to ensure you are ready for the transition. We also encourage you to speak with your TD Sales, Account or Relationship Manager for additional information.

For more information, we invite you to review the additional content on this site.

LIBOR Cessation Update

The USD LIBOR bank panel ended on June 30, 2023. Please refer to 'LIBOR Transition to SOFR' under 'Frequently Asked Questions' for more information about LIBOR cessation.

-

Frequently Asked Questions

-

Useful Links

-

Glossary and Key Terms

-

Other Resources

Overview

Benchmark Rate Reform (BRR) refers to the global initiative to transition major financial benchmarks – primarily Interbank Offered Rates (IBORs) – to alternative reference rates (ARRs). IBORs have played a central role in financial markets and act as reference rates to hundreds of trillions of dollars of derivatives and trillions of dollars in bonds, loans, securitizations and deposits. The dependence on IBORs by all sectors of the financial markets is now changing on a massive scale.

Why is the change necessary?

The need for BRR was brought to light by a lack of market liquidity underpinning IBORs which then enabled fraud and conspiracy scandals surrounding the London Interbank Offered Rate (LIBOR) during the 2008 financial crisis. In 2014, due to IBORs' sustainability concerns in the unsecured banking market, the Financial Stability Board (FSB) looked into risk-free reference rates (RFRs) as alternatives to IBORs. In 2017, the UK’s Financial Conduct Authority (FCA) announced that they will no longer compel or persuade banks to submit quotes to support most LIBOR currency settings after 2021 (and after June 30, 2023, for remaining USD LIBOR tenors).

As LIBOR’s cessation nears, global liquidity is shifting to products referencing ARRs, even in countries like Canada where LIBOR is not a predominant rate.

What will IBORs be replaced with?

BRR is primarily a business and market transformation initiative. Regulators have deferred to the industry to develop solutions for moving away from IBORs. The first step towards the IBOR transition was the designation of ARRs which have been selected to replace certain IBORs.

What is replacing IBORs?

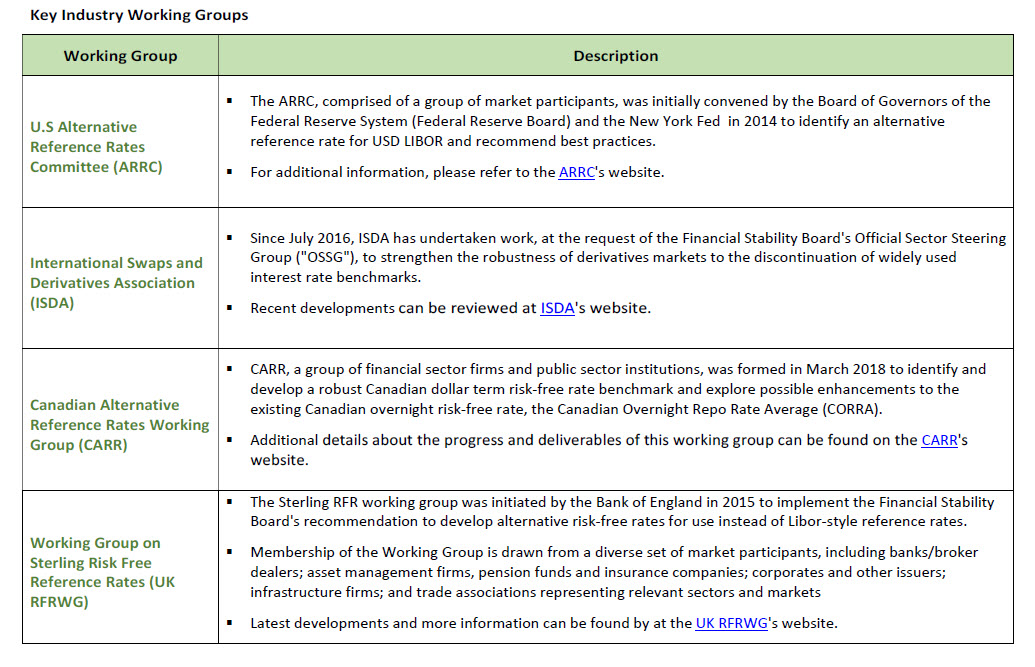

Key industry groups like the Federal Reserve Bank of New York’s (FRBNY) Alternative Reference Rates Committee (ARRC) in the U.S. and the Bank of Canada's (BoC) Canadian Alternative Reference Rate Working Group (CARR) have identified replacement ARRs and are assisting the industry with the transition. TD is actively participating in these industry groups to evaluate the recommendations and assess how we can best meet client needs.

Alternative Reference Rates by Region |

||||

Region |

Relevant Working Group |

Existing Benchmark |

Expected Discontinuation Date |

Alternative Risk-Free Rate |

Canada |

Canadian Alternative Reference Rate Working Group (CARR) |

CDOR |

July 1, 2024 May 17, 2021 |

Canadian Overnight Repo Rate Average (CORRA) |

United States |

Alternative Reference Rates Committee (ARRC) |

USD LIBOR |

January 1, 2022 July 1, 2023 |

Secured Overnight Financing Rate (SOFR) |

United Kingdom |

Working Group on Sterling Risk-Free Reference Rates |

GBP LIBOR |

January 1, 2022 |

Sterling Overnight Index Average (SONIA) |

European Union |

Working Group on Euro Risk-Free Rates |

EURIBOR, EONIA, EUR LIBOR |

January 1, 2022 |

Euro Short-Term Rate (€STR) |

Japan |

Cross-Industry Committee on Japanese Yen Interest Rate Benchmarks |

JPY LIBOR, JPY TIBOR, Euroyen TIBOR |

January 1, 2022 January 1, 2025 |

Tokyo Overnight Average Rate (TONA) |

Switzerland |

Swiss National Working Group |

CHF LIBOR |

January 1, 2022 |

Swiss Average Rate Overnight (SARON) |

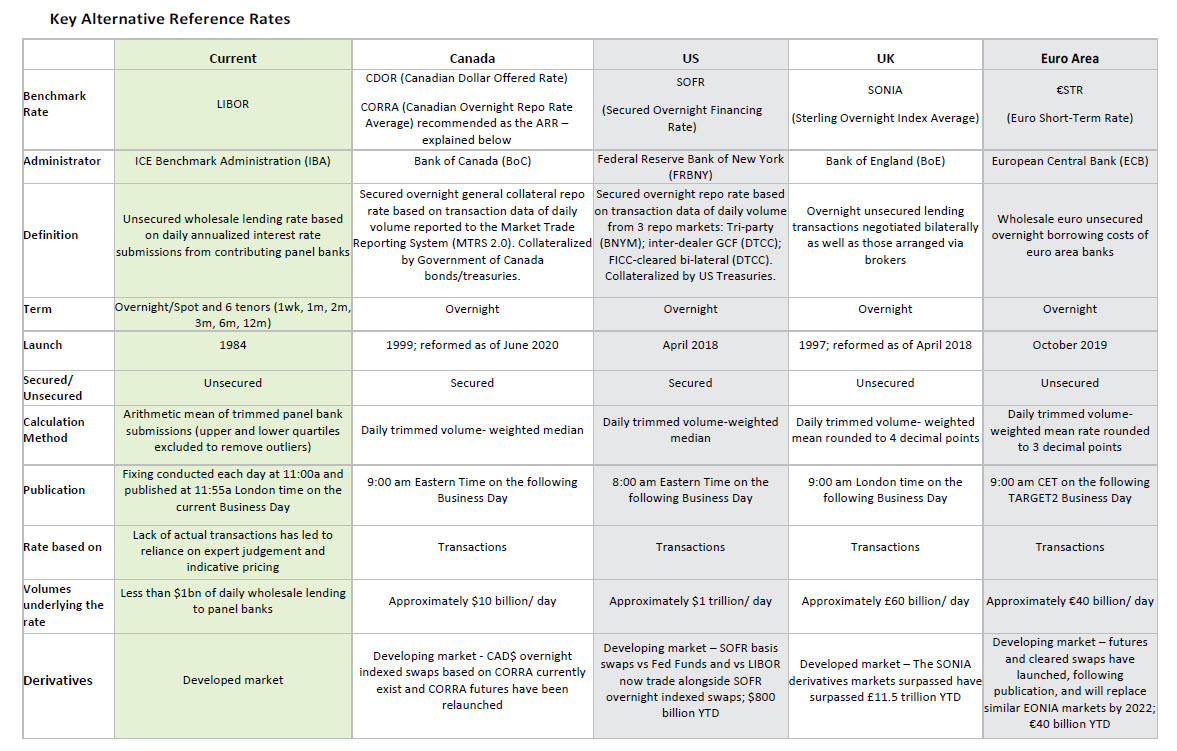

How do ARRs differ from IBORs?

There are several important key differences between IBORs and ARRs that make it necessary to develop both market conventions for the new ARR-based financial instruments and an approach to adjust for economic equivalence between the legacy IBOR and the replacement ARR at the time of transition.

IBORs |

ARRs |

IBORs carry a material credit risk component and hence generally trade at levels higher than ARRs. |

Most ARRs are based on overnight rates and carry virtually no credit risk component. Therefore, the margin applied to an ARR-based loan is usually larger than the margin on an otherwise identical IBOR-based loan, while the two would yield a similar all-in fixed rate. |

To reflect this difference, industry working groups have developed methodologies for including an adjustment to the replacement ARRs in fallback language of legacy IBOR contracts allowing the transition from IBOR to ARR to be performed in the most economically fair manner. |

ARRs also offer advantages in transparency and robustness as they are based on large volumes of actual executed transactions, while IBORs generally require use of interpolation and/or expert judgement to determine the current rate, as outlined in the chart below:

|

IBORs |

ARRs |

|

|---|---|---|

|

Feature: Administrator |

Private Sector / |

Central Banks / Central Bank regulated or prudentially regulated administrators |

|

Feature: Reset Mechanism |

Based on a narrow range of contributor banks' ability to borrow from each other for different terms |

Based on robust, very liquid underlying markets for overnight borrowing, reflecting actual transactions |

|

Feature: Publication |

Published on date T, in relation to underlying quotes |

Published on date T+1 for each currency (except SARON, on date T) |

|

Feature: Rate Term |

Tenors are generally published for terms which range from overnight to 12m |

Overnight rates |

How do I know if I have exposure to IBORs?

The transition impacts clients with IBOR-based products (e.g., cash or derivatives) maturing beyond a relevant benchmark cessation date.

Impacted clients are being contacted by their TD representative (as appropriate) to assist with the IBOR transition. It is recommended, however, that our clients seek independent legal, tax, and accounting advice to amend the terms of their IBOR-based floating rate commitments or to acquire new products that reference ARRs.

Below are a few examples of TD products that can be linked to IBORs:

|

Business Segment |

Products |

|---|---|

|

America's Most Convenient Bank (AMCB) |

|

|

TD Securities |

|

|

Commercial Business Banking |

|

|

TD Asset Management Inc. |

|

LIBOR Cessation

On June 30, 2023, the USD LIBOR bank panel ceased. From this date, USD LIBOR is now considered permanently unrepresentative of the underlying market it previously sought to measure. Working in partnership with our Customers, the vast majority of TD products referencing USD LIBOR have transitioned to indices based upon the Secured Overnight Financing Rate (SOFR) as recommended by US regulators, including CME Term SOFR Rates.

Under the US Adjustable Interest Rate (LIBOR) Act (the "Act"), in-scope USD LIBOR contracts governed by US law automatically converted to the relevant SOFR-based fallback rate if an amendment was not completed before July 1, 2023.

"Tough legacy" contracts that reference one or more of the 1-, 3-, or 6-month USD LIBOR settings and are not covered by the LIBOR Act may continue referencing a synthetic version of USD LIBOR, as published by ICE Benchmark Administration, through the end of September 2024. A small number of TD loan contracts are considered "tough legacy" as they cannot easily be amended to include a replacement rate for USD LIBOR and do not fall under the scope of the LIBOR Act. Synthetic USD LIBOR is calculated similarly to adjusted Term SOFR and is therefore not representative of unsecured bank lending markets. Other contracts may fallback to other specified rates.

TD is here to help if you have any questions or need assistance. As always, please reach out to your TD Relationship Manager.

Background

The Canadian Dollar Offered Rate (CDOR) is the rate at which banks are willing to lend to companies and is a recognized financial benchmark in Canada. It is determined daily from a survey of six principal market-makers including the major Canadian banks. CDOR is currently the primary interest rate benchmark in Canada and is widely used in other Canadian dollar financial instruments including interest rate swaps, exchange-traded futures, loans, and floating rate notes.

On March 5, 2021, ICE Benchmark Administration (IBA), the administrator of LIBOR, finalized its cessation plans and announced that most LIBOR settings would cease publication after December 31, 2021. The Federal Reserve Bank of New York’s (FRBNY) Alternative Reference Rates Committee (ARRC) recommended the Secured Overnight Financing Rate (SOFR) as its preferred RFR and endorsed the CME Term SOFR rates as the forward-looking index to replace USD LIBOR.

Why did ARRC select Term SOFR as the preferred rate for lending?

Term SOFR represents a market-based indication of the forward-looking measurement of overnight SOFR for one-, three-, six- and twelve-month periods. Term SOFR is based upon more than a trillion dollars in daily, reliably reported SOFR futures transaction volume.

By using Term SOFR, loans can be billed on a forward basis (i.e., for each one-month billing period, borrowers and lenders know the interest rate for that upcoming period and it is set at the beginning of the period).

TD Adopts SOFR-First Approach

TD has adopted a SOFR-first approach, selecting SOFR as the primary ARR for use in existing contracts priced at USD LIBOR. All new deals and most renewals are priced using SOFR. Because SOFR is a nearly risk-free index based on transactions secured by US treasuries, it has historically been a lower rate than USD LIBOR, which is unsecured and sensitive to market credit stress.

As of November 1, 2021, TD no longer issues new LIBOR products, except in certain, narrowly prescribed circumstances (e.g., market making or risk mitigation, etc.). Since 2022, the use of LIBOR in new transactions has been limited to these use cases. On June 30, 2023, the IBA will cease publication of all remaining USD LIBOR tenors (overnight, one month, three months and twelve months). This timing allows existing LIBOR contracts to mature or be modified to an alternative rate before LIBOR becomes unavailable.

LIBOR Cessation Timeline

Final panel bank submission dates are outlined in the following table:

|

Tenors |

Final Submission Date |

|

|---|---|---|

|

Currency: |

1-week, 2-month |

December 31, 2021 |

|

Currency: |

All other tenors |

June 30, 2023 |

|

Currency: |

All tenors |

December 31, 2021 |

Additional Information on LIBOR and SOFR

Please visit the following links for further information.

Background

On December 16, 2021, the Bank of Canada's (BoC) Canadian Alternative Reference Rate Working Group (CARR) released a white paper recommending that the administrator of CDOR – Refinitiv Benchmark Services (UK) Limited (RBSL) – cease publication of all three of CDOR’s remaining tenors after the end of June 2024. Following public consultation, RBSL announced that CDOR will cease to be published after a final publication on June 28, 2024. In response, the Office of the Superintendent of Financial Institutions (OSFI) published their expectations that federally regulated financial institutions (FRFIs) and federally regulated private pension plans (FRPPs) with transactions linked to CDOR make every effort to ensure a seamless transition to new reference rates, prior to the respective cessation dates.

What is CDOR?

CDOR stands for the Canadian Dollar Offered Rate and is currently the primary interest rate benchmark in Canada. It is a forward-looking survey-based benchmark measuring the average rate at which the six Canadian surveyed banks are willing to lend to corporate borrowers with existing committed Bankers’ Acceptance (BA) credit facilities. CDOR is a unique interest rate benchmark since it measures the average rate at which Canadian banks are willing to lend to corporate borrower while many other global credit sensitive rates, also known as interbank offered rates (IBORs), measure the rate at which banks are able to borrow.

CDOR is used for a variety of purposes, including to:

- Establish the floating-rate component of certain Over-the-Counter (OTC) and exchange-traded derivatives;

- Calculate interest payments on certain floating-rate notes and other securities; and

- Determine the base interest rate on certain loan agreements between corporate borrowers and banks.

CDOR currently comprises three tenors: 1 month, 2 months and 3 months. Two additional tenors, 6 months and 12 months, ceased to be published after May 14, 2021.

Why is CDOR Changing?

While CDOR has served the Canadian dollar market well for many years, there are certain aspects of CDOR’s architecture that pose risks to its future robustness as outlined in CARR's White Paper on the recommended future of CDOR. Key global interest rate benchmarks are increasingly being restructured to be based on large volumes of underlying transactions rather than expert judgement. CDOR is a lending rate which predominantly relies on expert judgement and cannot be directly tied to observable market transactions which is not consistent with evolving global best-practices.

CARR’s objective has been to analyze these issues in the context of the new, higher standards expected of critical interest rate benchmarks to ensure Canada’s benchmark regime is robust and resilient in the future. The findings and recommendations in the CDOR White Paper reflect global efforts to move from IBORs like CDOR to risk-free rates (RFRs) like the Canadian Overnight Repo Rate Average (CORRA). CARR's recommendation and the associated transition plan have been unanimously endorsed and supported by the members of CARR and the Canadian Fixed Income Forum (CFIF).

TD is adhering to CARR's recommendations for the CDOR to CORRA transition.

CARR's Two-Staged Approach to CDOR Transition

To prepare for CDOR’s cessation, CARR has recommended a two-staged transition approach, where derivatives and securities will transition from CDOR to CORRA by the end of June 2023, and loan contracts will transition starting November 1, 2023 up until the CDOR cessation date.

Stage 1 - Runs until June 30, 2023 |

Stage 2 - Ends June 28, 2024 |

|

|

Whenever possible, CARR recommends writing new contracts based on CORRA. For contracts that need to reference CDOR, CARR recommends incorporating robust fallback language provisions such that these contracts fall back to CORRA upon CDOR cessation.

What is CORRA?

The Canadian Overnight Repo Rate Average is well-known and has been a benchmark since 1997. The Bank of Canada (BoC) became CORRA’s administrator in 2019 and implemented a new calculation methodology developed by CARR.

Unlike CDOR, CORRA is based on actual transactions in the Canadian dollar overnight funding market, making it more robust and transparent than CDOR. Because the underlying transactions are collateralized by high-quality assets such as Government of Canada treasury bills, CORRA includes little or no credit risk component and is referred to as a risk-free rate.

CARR expects that the majority of the financial products (or exposure) currently referencing CDOR will transition to overnight CORRA calculated in-arrears. This is consistent with the practice in other jurisdictions. The importance of adopting overnight risk-free rates, where possible, has been underscored by the Financial Stability Board (FSB) as well as by the BoC and other central banks and regulators.

Term CORRA

The Term CORRA benchmark officially launched on September 5, 2023, in response to a strong demand from Canadian corporations for a forward-looking term benchmark.

Term CORRA is a forward-looking measurement of overnight CORRA for 1- and 3-month tenors, based on market-implied expectations from CORRA derivatives markets. The rate is calculated from 1- and 3- month CORRA futures trading on the Montréal Exchange using both transactions and executable bids and offers in the central limit order book over a specific calculation period. As a result, the robustness of the Term CORRA rates relies on the continued existence of a deep and liquid CORRA derivatives market based on overnight CORRA.

Term CORRA is intended to complement overnight CORRA and facilitate CDOR transition where transitioning from a forward-looking term rate (like CDOR) to an overnight rate is difficult. Term CORRA is an attractive replacement for CDOR because, like CDOR, Term CORRA allows borrowers and lenders to know the benchmark interest rate on a loan at the beginning (as opposed to near the end) of each interest period.

In endorsing the Term CORRA rates, the CARR recommended that its use remain limited, particularly in derivatives markets. Following CARR’s recommendations, CanDeal Benchmark Administration Services Inc. is restricting uses of Term CORRA (through its licensing agreement) to specific use cases, including loans, trade finance, and associated derivative hedges for those loans and CORRA-Term CORRA basis risk. Furthermore, CARR expects any users of Term CORRA to have robust fallback language in place that uses, in most cases, overnight CORRA calculated in-arrears, and to build the operational capacity to transact in these fallbacks should Term CORRA cease to be published in the future.

For more information and developments around Term CORRA, please refer to the following publications and websites

- CARR announces development of a Term CORRA benchmark

- Term CORRA Methodology - CARR Recommended Approach

- CARR’s approved use cases for Term CORRA

Will Bankers' Acceptances be impacted when CDOR is discontinued?

With the cessation of CDOR’s publication, the Bankers’ Acceptance (BA) based lending model, which is responsible for creating the BAs that are sold to money market investors, will be discontinued. TD is working with the Canadian Fixed-Income Forum (CFIF) as well as market participants to identify potential alternatives or replacements for Bankers' Acceptances.

BAs are a discount instrument whereby interest is paid upfront, and the borrower is advanced the discounted proceeds (principal loan amount less interest expense). CORRA loans, whether overnight CORRA or Term CORRA, will require the borrower to pay interest "in arrears", that is, at the end of the interest period.

Please refer to CFIF’s white papers on the Impact of CDOR Cessation on Bankers’ Acceptance Market and Update from the BA Transition Virtual Network for further information on the topic.

Additional Information on CDOR and CORRA

Canadian Alternative Reference Rate Working Group (CARR)

- Canadian Alternative Reference Rate (CARR) Working Group Website

- Canadian interest rate benchmark reform

- Recommended terms for CORRA-based loans

- CARR publishes White Paper on the recommended future of CDOR

- Refinitiv announcement of cessation of CDOR in June 2024

- OSFI’s expectations for CDOR Transition

- TMX CDOR Transition Webcast Series

- CARR announces development of a Term CORRA benchmark

- Term CORRA Methodology - CARR Recommended Approach

- Transitioning Loans from CDOR to CORRA – Best Practices

- Recommended CORRA loan agreement definitions and loan mechanics

- CORRA loan conventions comparison table

- CARR’s allowable use cases for Term CORRA

Refinitiv

OSFI

TMX

TD's enterprise-wide BRR Initiative provides support and strategic direction to all areas of the Bank impacted by the IBOR transition by offering new ARR-based products and actively engaging clients to transition existing ("legacy") products to ARRs.

TD is actively participating in industry working groups to help drive solutions and constantly adapting as market information becomes available. These groups include the Federal Reserve Bank of New York’s (FRBNY) Alternative Reference Rates Committee (ARRC) and the Bank of Canada's (BoC) Canadian Alternative Reference Rate Working Group (CARR).

TD also monitors information from other sources, such as the International Swaps and Derivatives Association (ISDA), the Working Group on Euro Risk-Free Rates led by the European Securities and Market Authority, and the Working Group on Sterling Risk-Free Reference Rates led by the Bank of England.

Up to date information from some of the key working groups focusing on benchmark rate reform can be found at:

|

Key Working Groups |

Details |

|---|---|

|

ARRC |

|

|

CARR |

|

|

ISDA |

|

|

Sterling RFR WG |

|

|

EUR RFR WG |

TD is working with clients throughout this transition

TD aims to provide clients with accurate, up-to-date information throughout the transition. Sales, Account, and Relationship Managers are actively engaging with clients to provide education and discuss contract amendments in a manner consistent with market directions as solutions are available and practical to implement.

What are the fallback provisions?

Various industry groups have provided fallback language for impacted financial products addressing permanent IBOR cessation. Clients should consider the economic and financial impact of the fallback provisions in their own contracts.

|

Term |

Definition |

|---|---|

|

Fallback Language |

Fallback language refers to the legal provisions in a contract that apply if the underlying reference rate in the product is not published (whether on a temporary or permanent basis). |

|

Hardwired Fallback Language |

Hardwired language provides that, upon an IBOR cessation trigger event (as defined in the agreement), the agreement will fall back to a waterfall of fallback rates and spreads. If the first option in the waterfall is unavailable, the contract will reference the next option in the list and so on. As a result, the fallback is hardwired into the contract and parties will not need to negotiate a new rate and spread upon a cessation event. |

|

Fallback Rate |

The reference rate replacing an IBOR upon the Fallback Trigger Event. The updated ISDA Definitions specify ARRs as compounded in arrear settings as replacement rates for derivative contracts referencing an IBORs. However certain cash product contracts may contain no suitable language, resulting in the contracts falling back to the last IBOR setting or the lenders' costs of funds. |

|

Spread Adjustment |

As noted, IBORs are different to the ARRs applicable in each jurisdiction and as part of ISDA fallback methodology a fixed spread adjustment is applied to the ARR to account for differences in the construction of the IBOR and the ARR. |

|

Fallback Trigger Event |

Set of events relating to the original reference rate which may trigger the fallback to a new reference rate. |

Is there an industry solution to assist with the amendment of derivative agreements?

Yes. On January 25, 2021, the International Swaps and Derivatives Association (ISDA) 2020 IBOR Fallbacks Protocol and the ISDA IBOR Fallbacks Supplement became effective. Any transactions incorporating the 2006 ISDA Definitions that were entered into on or after January 25, 2021, will automatically include updated fallback language. Any transactions incorporating the 2021 ISDA Interest Rate Derivatives Definitions will also automatically include updated fallback language. Transactions entered into prior to January 25, 2021, known as legacy transactions, will not be automatically amended. To facilitate amendment of legacy transactions, both parties to the transaction need to adhere to the ISDA Protocol or bilaterally amend fallback language in the derivative agreement.

TD is working with clients to update fallback language in IBOR agreements

Following guidance from the Federal Reserve Bank of New York’s (FRBNY) Alternative Reference Rates Committee (ARRC) and the Bank of Canada's (BoC) Canadian Alternative Reference Rate Working Group (CARR) and other industry groups, and in line with market practice, TD aims to include fallback language in any new agreement or agreements undergoing renewal or refinancing and the "hardwired" approach for syndicated loans and lender discretion language for bi-lateral loans.

We do our best to meet an individual client's needs while ensuring all clients are treated in a fair and consistent manner. For some cash products, the "amendment" approach may remain appropriate.

Additional Information on Fallbacks and Fallback Language

Accounting and tax bodies have developed guidance to address the implications related to legacy contract transitions from IBOR to new ARRs. The general objective of the guidance is to provide accommodations for the move from IBORs to ARRs to mitigate unintended consequences, such as net income volatility or termination of certain hedge accounting relationships.

Clients will need to identify the changes made to their contracts to assess if they fall within the explicit guidance of the relevant body in their jurisdiction to determine the accounting and tax impacts. Clients should engage their legal, tax and accounting advisors for guidance.

|

Term |

Definition |

|---|---|

|

BRR |

Benchmark Rate Reform; the transition from Interbank Offered Rates (IBORs) to Alternative Reference Rates (ARRs) |

|

Fallback Language |

Contractual provisions that set out the process for identifying when a replacement to the specified interest rate should be used and what it should be |

|

SOFR |

Secured Overnight Financing Rate. SOFR was recommended by ARRC as a replacement for USD LIBOR (versus alternative IBORs) on the basis of the depth of the underlying market and its likely robustness over time. Unlike LIBOR, SOFR is an overnight rate, not a term rate. SOFR is a broad measure of the cost of borrowing cash overnight, collateralized by U.S. Treasury securities, calculated by a volume- weighted median of this transaction-level data. |

|

IBORs |

Interbank Offered Rates; the interest rate that banks in a jurisdiction charge one another for short-term, interbank loans. |

|

LIBOR |

London Interbank Offered Rate; arguably the most important Interbank Offered Rate (IBOR) used in the global financial market and serves as a key interest rate benchmark across a number of financial products including derivatives, securities, loans and mortgages. |

|

FCA |

Financial Conduct Authority; the conduct regulator for nearly 60,000 financial services firms and financial markets in the UK and the prudential supervisor for 49,000 firms, setting specific standards for 19,000 firms. |

|

ARRs |

Alternative Reference Rates; benchmark interest rate used to determine other interest rates. |

|

ARRC |

Alternative Reference Rates Committee; group of private market participants convened by the Federal Reserve Board and the New York Fed to help ensure a successful transition from U.S. dollar (USD) LIBOR to a more robust alternative reference rate. |

|

FRBNY |

Federal Reserve Bank of New York |

|

ISDA |

International Swaps and Derivatives Association; a trade organization created by the private negotiated derivatives market that represents participating parties and helps to improve the private negotiated derivatives market by identifying and reducing risks in the market. |

|

CARR |

Canadian Alternative Reference Rates Working Group; created to identify and seek to develop a new term risk-free Canadian dollar interest rate benchmark |

|

SONIA |

Sterling Overnight Index Average benchmark; the effective overnight interest rate paid by banks for unsecured transactions in the British sterling market. |

|

FRNs |

Floating Rate Notes; bonds which reference a floating rate for the determination of payments. |

|

Market conventions |

Prevalent practice in the relevant Interbank Market ; designed to mirror the consensus view of the market as to the current accepted practices in the respective markets and to help avoid misunderstandings. |

|

CDOR |

Canadian Dollar Offered Rate; rate at which banks commit to lending to companies. |

|

CORRA |

Canadian Overnight Repo Rate Average |

|

AMCB |

America's Most Convenient Bank |